Markets & Economy

Categories

Global Equities

2021 Outlook: Turning points on the road to recovery

Jody Jonsson

Jody Jonsson

Jared Franz

Jared Franz

Mike Gitlin

Mike Gitlin

December 15, 2020

With the wreckage of 2020 in the rearview mirror, investor optimism for the new year is high. After all, how could it possibly be any worse than a year marked by a deadly pandemic, a brutal recession and one of the steepest bear markets in history?

In contrast, 2021 is poised to be a critical turning point on several fronts — whether it’s the vaccine-assisted defeat of COVID-19, the resurgence of global economic growth, or the transformation of how we live and work in the digital age.

“At the start of the pandemic, who would have thought that nine months later markets would be making new highs?” says Capital Group portfolio manager Jody Jonsson. “We still have a long way to go and there is still a lot of suffering around the world, but I think we are at a point now where we can clearly see the end of this crisis and the foundations of a sustainable recovery.”

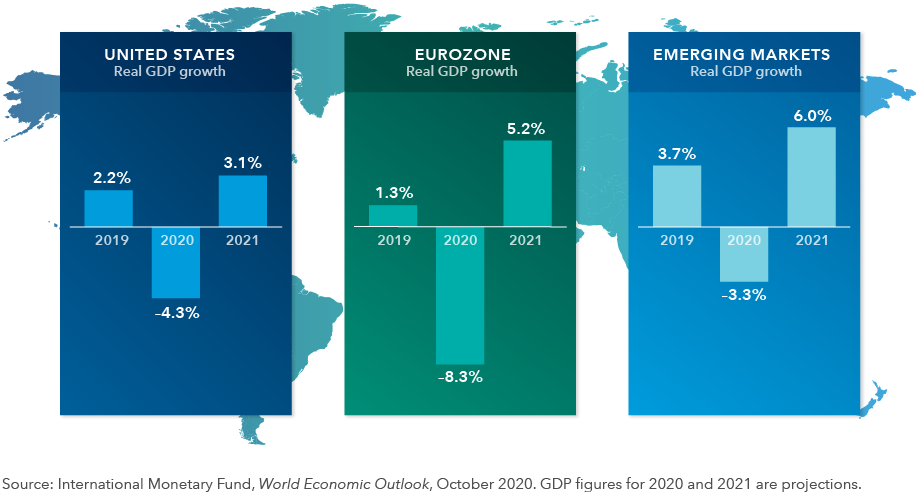

The world is turning the corner toward recovery

Equity markets have been predicting such an outcome for months, rallying in the face of government-imposed lockdowns and dire economic numbers. On a year-to-date basis, the MSCI World Index is up more than 11%, as of mid-December, led by surging technology and e-commerce stocks. Emerging markets stocks have done even better, fueled by China’s first-in first-out recovery from the COVID crisis.

A critically important announcement came on December 11 when the U.S. Food and Drug Administration granted emergency use authorization for a COVID-19 vaccine developed by Pfizer and BioNTech, paving the way for mass inoculations to begin this week. Pfizer has said it plans to distribute 25 million doses in the U.S. by the end of the month.

With these events in mind, the outlook for 2021 is coming into sharper focus. Many Capital Group investment professionals remain optimistic for the year ahead:

2021 Outlook webinar

Get insights for 2021 and beyond

CE credit available

U.S. outlook: The future is here, and it’s digital

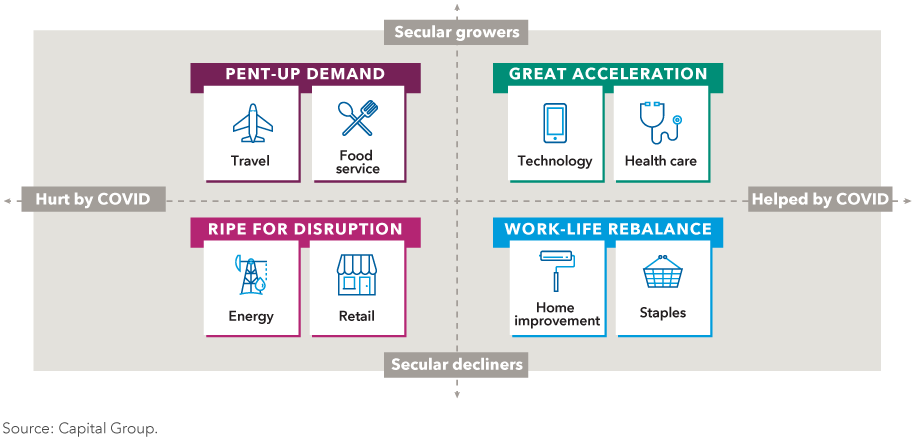

Every so often a crisis comes along that drives change at such velocity that investors can almost feel the ground shift beneath their feet. That happened in 2020 as the pandemic forced companies to prioritize and expand their online operations. Those without a digital advantage found themselves left behind.

For restaurants, hotels, retailers, airlines and small businesses, it has literally been the worst of times. At the opposite end of the spectrum, the stay-at-home era has been a boon for e-commerce, cloud computing, video streaming, digital payment processors and home improvement stores. The key question now is: How much of that activity was purely COVID-driven, and how much of it will persist in the years ahead?

A framework for evaluating COVID winners and losers

“The post-pandemic economy is going to look very different than the one we had in February 2020,” says Capital Group economist Jared Franz. “It’s going to be more efficient and more dynamic, but there will be winners and losers. Our job as active investors is to identify them — finding the growing companies that have not only benefited from the pandemic but that also have the potential to continue generating solid growth in a post-pandemic world.”

If the U.S. can swiftly administer millions of COVID vaccines by midyear, Franz believes U.S. economic growth could rise to roughly 3% on an annualized basis. That would be one of the strongest U.S. GDP readings of the past decade.

International outlook: Innovation isn’t just a U.S. story

Digital business models have certainly thrived in the U.S., but investors would do well to look beyond geographical borders to find some of the most innovative companies in the world.

Asian companies, for instance, have rapidly adopted digital payment technologies on a wide scale and, in many respects, the U.S. is playing catch-up. Simply put, cash is no longer king in many non-U.S. markets.

In some emerging markets just a few years ago, many customers had no bank accounts but did have mobile phones — and that led to faster adoption of mobile payments. In China, Alipay (part of Ant Financial) and Tenpay (run by Tencent) are dominant players. Others also have grown rapidly, including Yeahka in China and PagSeguro and StoneCo in Brazil, which provide mobile payment platforms for merchants.

Asia has become the world leader in digital payments

.png)

This powerful trend is another reminder why investors shouldn’t ignore opportunities in international and emerging markets. While the U.S. is likely to remain a primary engine for innovation, it would be shortsighted to think of the U.S. as the sole province of inventive companies. What’s more important for investors is to seek out the world’s most innovative companies in growing industries wherever they are located.

Fixed income outlook: Bonds in a bumpy recovery

The unprecedented stock market turmoil of 2020 has made one thing abundantly clear: High-quality bonds are not just a potential source of steady and reliable income, they can also perform a crucial task during times of extreme crisis.

In the opening weeks of 2020, some bond bears argued that with most U.S. Treasury yields below 2%, fixed income investments offered little value and might no longer serve as an effective hedge against stocks. Once again, these predictions proved wrong.

In the depths of the bear market while U.S. stocks, as measured by the Standard & Poor’s 500 Composite Index, declined more than 30%, the Bloomberg Barclays U.S. Aggregate Bond Index, a typical benchmark for core bond funds, did exactly what it was supposed to do. It zigged when stocks zagged, providing both diversification and capital preservation. And even as equities have recovered, bonds have held up. The benchmark was up 7.4% as of November 2020.

The core bond benchmark held steady as stocks sank

.png)

“In this challenging market environment, high-quality fixed income has shined,” says Mike Gitlin, Capital Group’s head of fixed income. “Anyone who held a strong core fixed income allocation should be more convinced than ever of its value — and its role in a balanced portfolio.”

Learn more about

Standard & Poor’s 500 Composite Index is a market capitalization-weighted index based on the results of approximately 500 widely held common stocks.

Bloomberg Barclays U.S. Aggregate Index represents the U.S. investment-grade fixed-rate bond market.

MSCI World Index is a free float-adjusted market capitalization-weighted index that is designed to measure equity market results of developed markets.

The market indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index.

Investing outside the United States involves risks, such as currency fluctuations, periods of illiquidity and price volatility, as more fully described in the prospectus. These risks may be heightened in connection with investments in developing countries. Small-company stocks entail additional risks, and they can fluctuate in price more than larger company stocks.

The return of principal for bond funds and for funds with significant underlying bond holdings is not guaranteed. Fund shares are subject to the same interest rate, inflation and credit risks associated with the underlying bond holdings. Lower rated bonds are subject to greater fluctuations in value and risk of loss of income and principal than higher rated bonds.

Bloomberg® is a trademark of Bloomberg Finance L.P. (collectively with its affiliates, “Bloomberg”). Barclays® is a trademark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Neither Bloomberg nor Barclays approves or endorses this material, guarantees the accuracy or completeness of any information herein and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

©2020 Morningstar, Inc. All rights reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.

The Standard & Poor’s 500 Composite Index is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2020 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

RELATED INSIGHTS

-

-

Asset Allocation

-

Never miss an insight

The Capital Ideas newsletter delivers weekly insights straight to your inbox.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the mutual fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only. Use of this website and materials is also subject to approval by your home office.

Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.