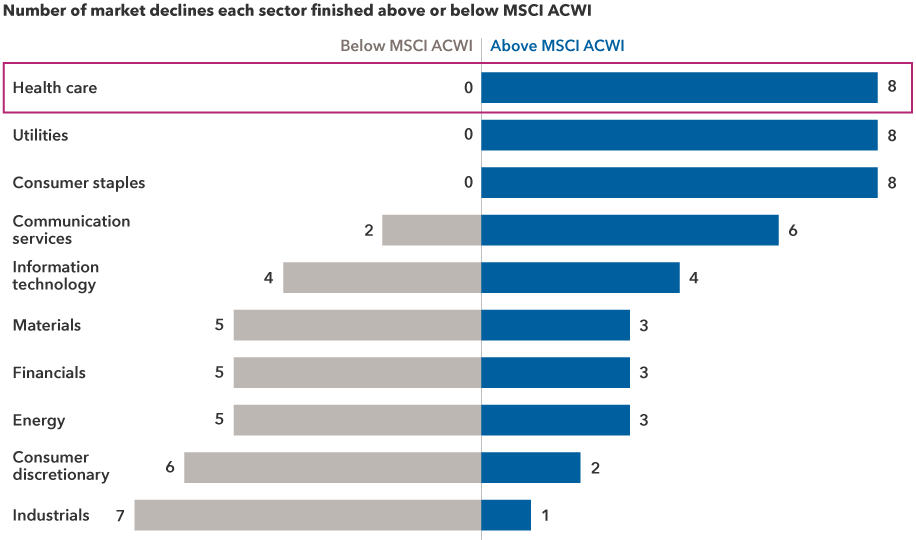

Amid the storm of market volatility in the first half of 2022, health care was among the few areas that offered investors some shelter.

That may not be surprising, considering that demand for services in the sector tend to hold up regardless of market volatility or the economic cycle. In fact, the sector has outpaced the broader global stock market in each of the past eight market declines of 15% or more.

Indeed, prospects for select companies appear to be brightening, and some have the potential to remain compelling investment opportunities for years to come, according to equity analyst Christopher Lee, who covers U.S. pharmaceuticals and biotechnology companies.

“Health care has been a good place to invest since the start of the pandemic for a variety of reasons,” says Lee, who holds a medical degree from Columbia University. “First you had biopharma companies developing vaccines and treatments for COVID. Now you have other companies benefiting from their defensive nature in a time of uncertainty in the markets.”