Chart in Focus

Categories

United States

5 realities of this recession

Darrell Spence

Darrell Spence

April 29, 2020

Recessions can be hard to predict, but that’s not the case this time. The COVID-19 pandemic sweeping the globe has pushed the U.S. economy into recession, with U.S. GDP falling 4.8% in the first quarter. While the drop was sizable, an even more pronounced decline is in store for the second quarter, as broad swaths of the country remain shuttered. With the U.S. feeling the sting of a sharp reduction in consumer spending and industrial production, there are five realities to keep in mind.

1) We’ve been here before (sort of)

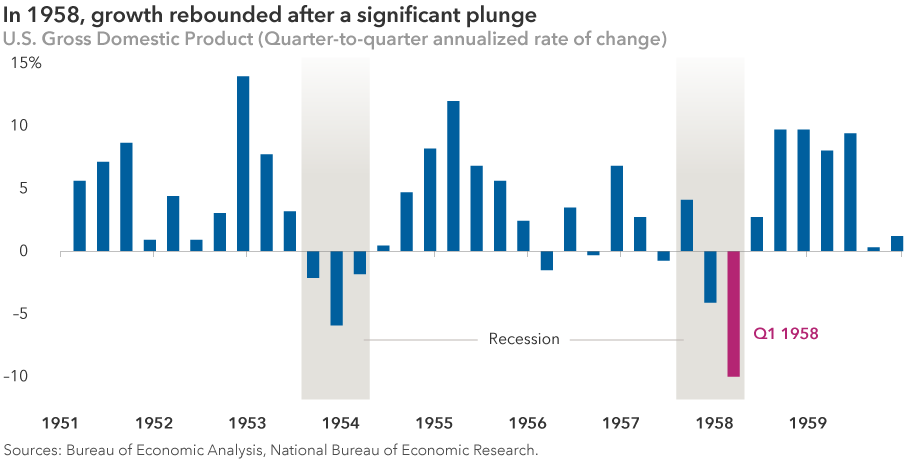

The largest post-1950 quarterly GDP decline was 10% in the first quarter of 1958.

This sharp drop in growth came amid the 1957–1958 recession, which resulted from a confluence of factors, including a flu pandemic. While the makeup of the present-day economy is much different, the U.S. is not unfamiliar with pandemic-related economic turmoil. The U.S. economy bounced back strongly in the late 1950s, with growth surpassing 5%.

As parts of the U.S. look to ease restrictions, I believe that a bounce back in activity could begin as early as June in some sectors and more broadly in the third quarter.

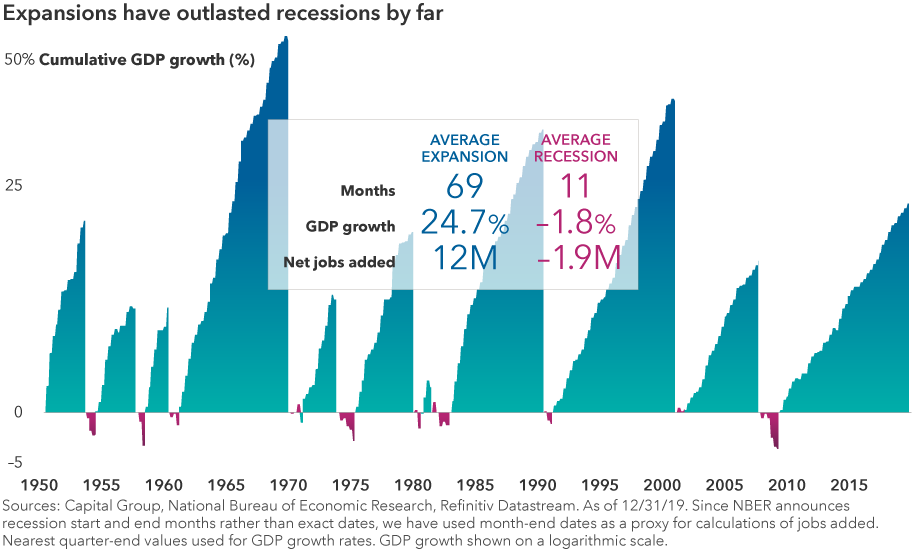

2) Recessions have tended to be short; the subsequent expansions have been powerful

The good news is that recessions generally haven’t lasted very long. While this time may be different, our analysis of 10 cycles since 1950 shows that recessions have ranged from eight to 18 months, with the average lasting about 11 months. For those directly affected by job loss or business closures, that can feel like an eternity. While there's no way to minimize that feeling, investors with a long-term investment horizon should try to look at the big picture. The average expansion increased economic output by 25%, whereas the average recession reduced GDP by less than 2%.

3) It’s about the consumer

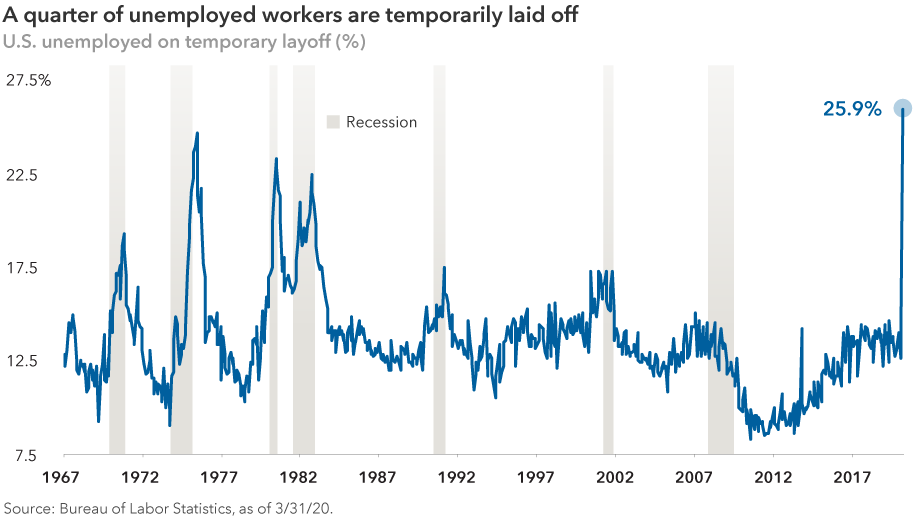

The U.S. consumer accounts for approximately two-thirds of the economy. With unemployment claims skyrocketing — although many may be temporary — and consumers staying in their homes, a weakening economy is no surprise. The $2 trillion stimulus package will help support some levels of consumer activity, but employment uncertainty is likely to keep many consumers in a frugal mindset.

4) Lower oil prices may be a tailwind for the economy

A precipitous decline in crude oil prices has put pressure on the energy sector. May oil contracts turned negative in April as producers scrambled to find storage for bloated supply stores, exacerbated by consumers’ sharp reduction in vehicle usage and gasoline consumption. While the negative impact of lower oil prices is likely to be felt in U.S. oil fields, lower energy prices can provide a tailwind for consumers and transportation-heavy industries.

5) Timing may not be everything

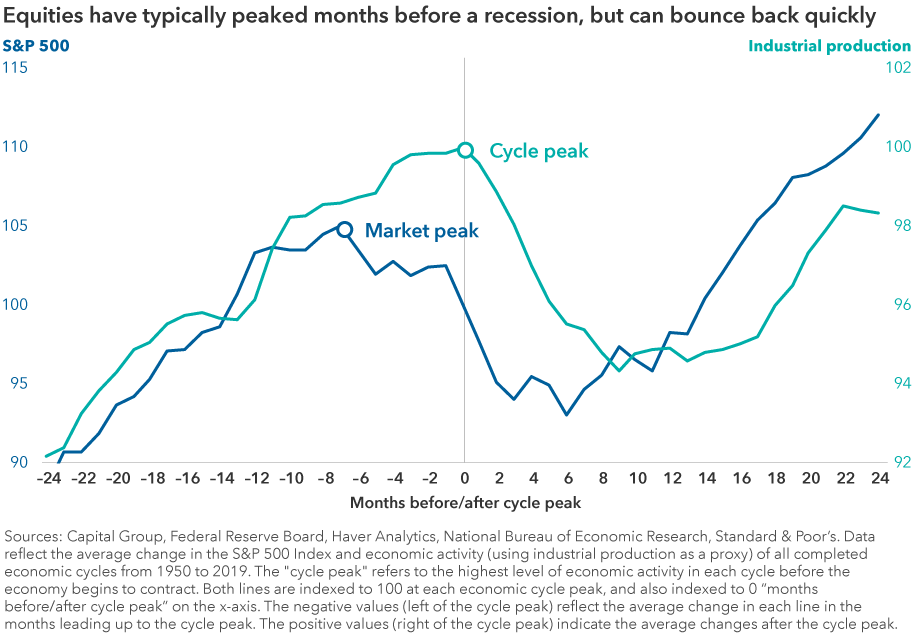

Waiting for the all-clear may leave investors missing out on market gains. Since World War II, in recessions with a corresponding equity correction, the S&P 500 has bottomed, on average, three months before the end of each recessionary period. It’s little solace to investors who have endured market volatility, but even as the economy weakens, there are opportunities to invest in great companies at a discount.

While the adage that the stock market is not the economy is true, market volatility tends to be captured, with a lag, in economic data. So even as financial markets are on a path to recovery, it may take time for the economy to catch up. Focusing on long-term investing can help investors navigate short-term volatility.

For more insights into recessions, check out our updated Guide to Recessions.

Learn more about

The Standard & Poor’s 500 Composite Index is a market capitalization-weighted index based on the results of approximately 500 widely held common stocks. The S&P 500 is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2020 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

Our latest insights

-

-

Economic Indicators

-

Demographics & Culture

-

Emerging Markets

-

Never miss an insight

The Capital Ideas newsletter delivers weekly insights straight to your inbox.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the mutual fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only. Use of this website and materials is also subject to approval by your home office.

Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.