Chart in Focus

Categories

Aerospace

Air travel is taking off again

Todd Saligman

Todd Saligman

Steve Watson

Steve Watson

Christopher Thomsen

Christopher Thomsen

May 10, 2022

After two years of relatively empty skies, Ryanair CEO Michael O'Leary is an eyewitness to the incredible resurgence of demand for air travel. Faced with long security delays at Dublin Airport, he implored the Irish government to call up the army last month to help process eager travelers flooding the terminals.

As the global economy gradually emerges from the pandemic, airports around the world are dealing with a crush of passengers looking to make up for lost time. Fueled by pent-up demand, many are flying for the first time since the COVID-19 virus crippled the travel industry. For the airlines, the turnaround in demand has been fast and furious, surpassing even the most optimistic expectations.

“Demand is turning back on almost as quickly as it turned off,” says Capital Group equity analyst Todd Saligman, who covers the aerospace industry in the U.S. and Europe. “Many U.S. airlines have reported that March was the strongest booking month in history, and we are seeing similar strength in Europe.”

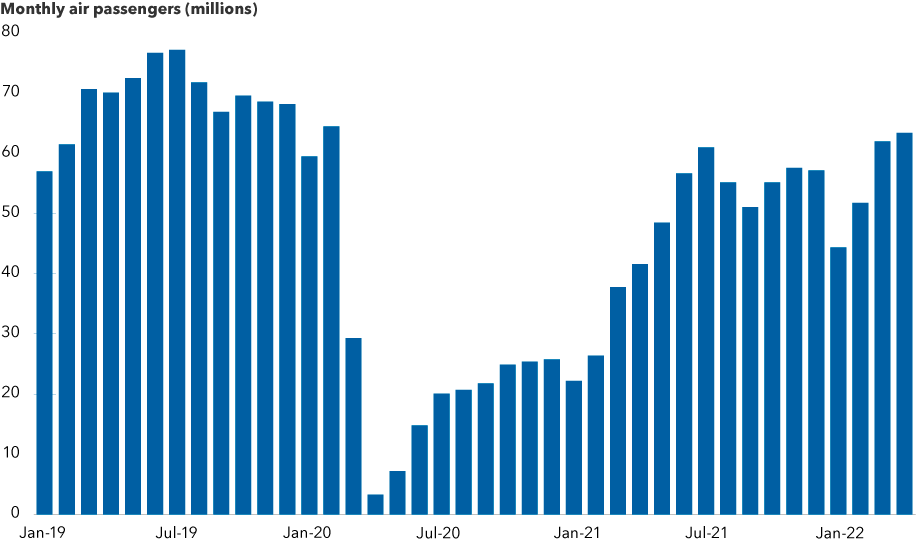

U.S. air travel is rebounding from a sharp pandemic-era downturn

Sources: Capital Group, U.S. Transportation Security Administration. Data reflects number of travelers going through TSA airport checkpoints. As of 4/30/22.

Heading into the summer vacation season, air travel is likely to exceed pre-COVID levels in much of the Western world. That’s despite several headwinds facing the airlines today, including sharply higher fuel costs, a pilot shortage and fewer available flights as the industry ramps up to full strength. A resurgence of the virus is holding back China’s reopening, leaving Asian air travel lagging the U.S. and Europe at the moment.

“We’re not back to pre-COVID levels yet, but it’s just a matter of time,” Saligman notes. “Travel is a secular growth industry in a lot of countries. Only about 20% of the world’s population has ever been on an airplane. So there is huge room for growth, especially in emerging markets such as China and India, where the middle class is growing and air travel is still in its infancy.”

Capital Ideas™ webinars

Insights for long-term success

CE credit available

Volatility is in the air

Make no mistake, airline stocks are volatile. As a group, U.S. airline stocks fell 31% in 2020 as government-imposed lockdowns and bans on international travel brought air traffic to a virtual standstill. They fell another 2% in 2021, even as a reawakening economy lifted other sectors. It’s been a mixed bag so far this year, with the sector up nearly 10%, despite a pullback after Russia’s February 24 invasion of Ukraine.

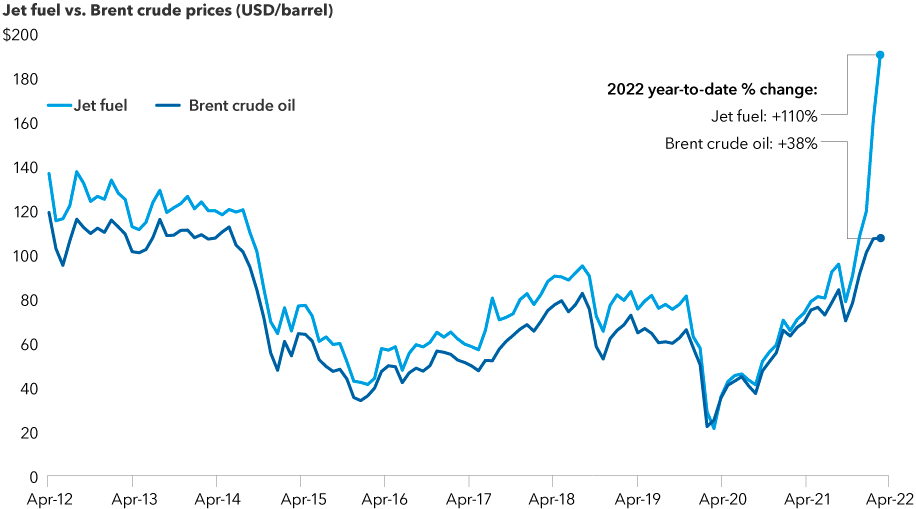

The war has contributed to a meteoric rise in the price of jet fuel, which has increased 110% this year, surpassing the rise in oil prices by a wide margin. Fuel is generally the second largest expense for airlines, after labor.

Jet fuel costs are rising even faster than oil prices

Sources: Capital Group, Refinitiv Datastream. Jet fuel prices represented by the U.S. Gulf Coast Kerosene-Type Jet Spot Price; Brent crude prices represented by the Europe Brent Spot Price. As of 4/30/2022.

In normal times, such a dramatic increase in jet fuel prices would hurt the highly competitive aviation industry. But these aren’t normal times.

“Airlines have largely been able to pass these costs along in the form of higher airfares,” Saligman explains. “These stocks will likely continue to be volatile, but I think the next six to 12 months could be a very strong period for the airlines, as well as cruise lines and other travel-related companies.”

Indeed, two of the largest U.S. carriers — American Airlines and Delta Airlines — are both forecasting record-high revenues in the current quarter ending June 30. In recent earnings calls, airline executives said they expect sales to soar during the summer travel season. “Demand is stronger than I’ve ever seen in my career,” said United CEO Scott Kirby, “and that’s even before business travel fully recovers.”

Airline industry poised for rapid growth in a post-pandemic world

Sources: Capital Group, MSCI, Refinitiv Datastream, RIMES. As of 4/30/22.

Come fly with me

Optimism for the airline industry comes with a few caveats. The recovery should proceed if energy prices don’t continue to skyrocket, the Russia-Ukraine conflict doesn’t spread and severe COVID restrictions aren’t once again imposed. Those are some big assumptions that may or may not play out according to plan. But over the long term, the outlook is favorable, says Steve Watson, a portfolio manager with New Perspective Fund®.

“I think COVID will go away, and people will want to fly again — it’s that simple,” says Watson, who holds airlines, cruise lines and booking companies in his portfolios. “Investors should focus less on the timing and more on what cash flows and earnings will look like in the months and years ahead.”

What about the fear that Zoom or Webex video calls will replace the need for in-person business meetings? That’s nonsense, Watson says.

“Years ago, conference calls were supposed to kill business travel and that never really happened either,” he notes. “People who generate revenue face-to-face will be traveling.”

Long runway for “reopening” theme

As one of the few industries that has not fully participated in the COVID recovery period, many airlines are attractive from a valuation perspective, says Chris Thomsen, a portfolio manager with the EuroPacific Growth Fund®.

Airlines have experienced a delayed recovery, largely due to the emergence of the COVID-19 omicron variant last December. With omicron fading in many parts of the world, airlines and other travel-related companies are well positioned to participate in the comeback that has lifted other sectors hard hit by the 2020 downturn.

Thomsen saw evidence of that on a recent trip from London to Los Angeles.

“The airports were crowded, restaurants were bustling and flights were full,” he says. “I think we are in a post-COVID world now. People want to get out and do all the things they couldn’t over the past two years. That’s going to benefit the travel industry for the next few years at least.”

Learn more about

Latest insights

-

-

Economic Indicators

-

Demographics & Culture

-

Emerging Markets

-

RELATED INSIGHTS

-

International

-

-

Russia-Ukraine Conflict

Never miss an insight

The Capital Ideas newsletter delivers weekly insights straight to your inbox.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the mutual fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only. Use of this website and materials is also subject to approval by your home office.

Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.