Chart in Focus

Categories

Inflation

Pricing power can help companies fight inflation

Diana Wagner

Diana Wagner

October 26, 2021

Remember in 2011 when Netflix raised prices by dividing its streaming subscriptions from its DVD service? The announcement sparked an uproar that forced the company to issue an apology and hammered the stock price.

Today the world is in a very different place — and so is Netflix: The company is now a dominant streaming service and a megahit-making machine with more than 213 million subscribers worldwide. Its latest breakout, “Squid Game” — a Korean drama about children’s games played with deadly consequences — captivated some 142 million households, making it the most viewed show in Netflix history.

This rising popularity has empowered the company to boost its prices. It has increased subscription rates in the U.S. four times since 2014, a period of robust subscriber growth globally. This is an example of pricing power, the ability to increase prices without losing customers.

Pricing power can be an antidote for inflation

Pricing power, always a positive for companies that can sustain it, may be a crucial competitive advantage in the year ahead. Inflation has surfaced in the economy, and there are signs that it could linger in the coming months. The annual inflation rate in the U.S., as measured by the consumer price index, rose to 5.4% in September, its highest level in 13 years. Rising costs can erode a company’s profit margins and, ultimately, investor returns. But companies with clear, sustainable pricing power can protect their profit margins by passing those costs along to customers.

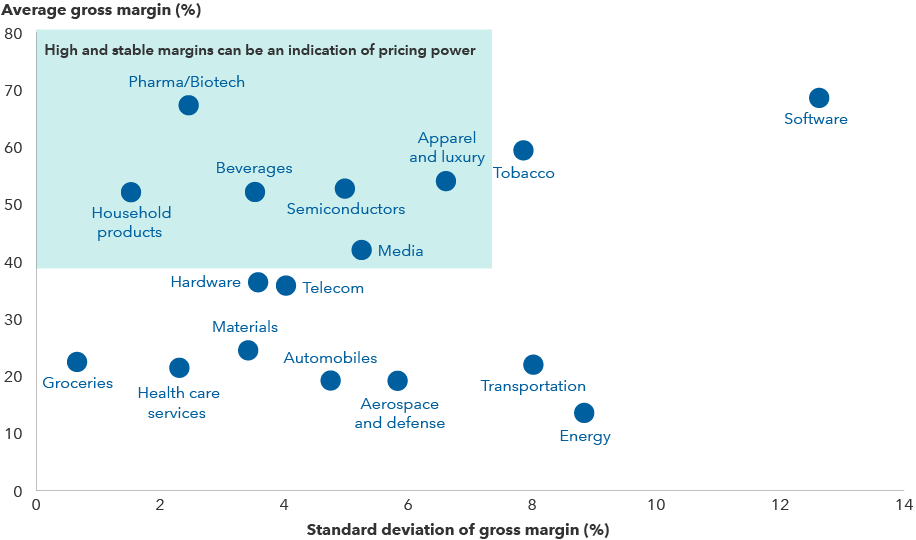

In some industries, there is greater potential for pricing power

Sources: Capital Group, FactSet, MSCI. Reflects industries within MSCI World Index. Average and standard deviation of gross margins are calculated for the five-year period ended 9/30/21.

With growth slowing and inflation pressures building, as an equity portfolio manager for Washington Mutual Investors FundSM, I think it is essential to understand how companies with pricing power can offset inflation. Here is my perspective on pricing power.

Health care services: A prescription for inflation’s ills

High medical costs are a perennial hot button issue in Washington, and for good reason. Over the last 20 years, health care costs have risen at about 2.5 times the rate of broad inflation, as measured by the PCE inflation rate followed by the U.S. Federal Reserve.

Historically, health insurance companies have had pricing power and passed on rising health care costs to their customers through higher premiums. Today, companies like UnitedHealth Group are no longer mere toll collectors on the freeway of rising health care costs. They actually manage care.

Consider UnitedHealth Group, which is focused on helping governments and health care providers reduce spending and improve outcomes for patients. The company has been investing in predictive analytics and care delivery to reduce inefficiencies in the U.S. health care system.

They determined that the most powerful person in the care delivery ecosystem is the primary care doctor, who represents 3 cents of every dollar we spend on health care but determines where another 85 cents is spent. By getting primary care doctors involved earlier in decisions about care, UnitedHealth is seeking to keep members healthy and get more value for every dollar spent. By delivering more value, UnitedHealth can maintain its pricing power while helping to tackle a long-term problem in this country.

You've discovered one of Capital Group's 10 investment themes for 2022

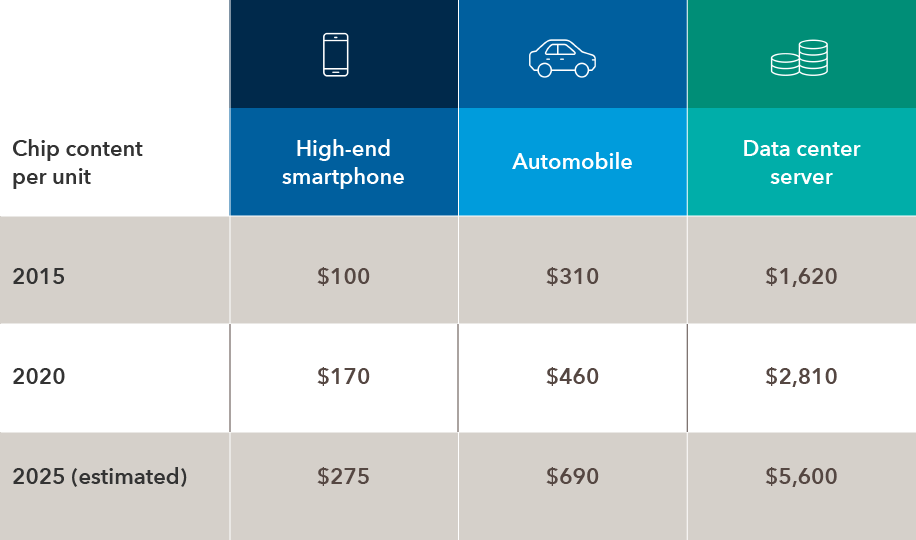

Semiconductors: Everywhere, in everything

The story of pricing power in the semiconductor industry is simple: Soaring demand meets limited supply. Today semiconductors can be found not only in mobile phones and laptops but also in everyday household products like refrigerators and ovens. New cars can require as many as 100 chips. Indeed, the auto industry has felt the brunt of the global shortage in semiconductor supply.

The rollout of new technologies, like 5G, artificial intelligence and cloud computing have further fueled the world’s appetite for chips. In August, Taiwan Semiconductor Manufacturing disclosed that it would raise chip prices by as much as 20%.

Consolidation in the semiconductor industry has transformed the competitive landscape, leaving a few dominant players with potential pricing power in specialized areas of the market. For example, companies with proprietary chip designs, like Broadcom, or Dutch chip-component manufacturer ASML, could raise their prices in an inflationary environment.

Demand for semiconductors is soaring — along with pricing power

Sources: Applied Materials, Capital Group. Figures for 2025 are estimated. All figures are in USD.

Beverages: Thirsty for leading brands

The ability to raise prices without serious backlash not only varies across industries but also within them. In the food and beverage industry, drink companies tend to pass along higher costs to consumers better than many food companies. That’s because the beverage industry is dominated by a few players with strong brand recognition.

Capital Ideas™ webinars

Insights for long-term success

CE credit available

One example is Keurig Dr Pepper, the producer of sodas and single serving coffee pods. The company has a history of pricing power, particularly for its most popular soft drinks, which include Canada Dry, Snapple and, of course, Dr Pepper.

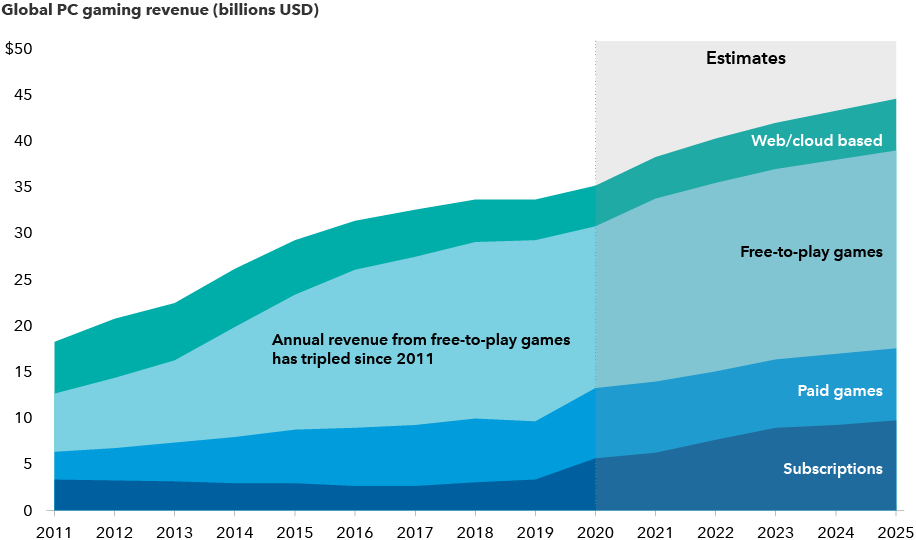

Video games: Not just child’s play

Once considered a minor niche in the entertainment industry, video games have soared in popularity and now represent the fastest growing segment of the world’s media entertainment industry. The global gaming industry is expected to grow to $225 billion in annual revenue by 2025.

Manufacturers have recently been flexing their power to raise prices. With Microsoft and Sony introducing updates to their Xbox and PlayStation consoles, respectively, game makers have disclosed plans to raise prices on console games to help account for the cost of creating more sophisticated games.

A prime example of pricing power potential in the industry is the annual revenue from free-to-play games like Apex Legends from Electronic Arts and Fortnite, published by Epic Games. Tencent has a 40% ownership stake in Epic. Activision owns King, the publisher of popular mobile game Candy Crush. Free-to-play games generate revenue through advertising, whose rates can be increased as costs go up and through in-game purchases.

Believe it or not, players spend real money on virtual clothing, weapons and other supplies for their gaming characters. Essentially, industry leaders can set the price for such items as they please.

Revenue from free-to-play games, an area of pricing flexibility, has soared since 2011

Sources: Capital Group, IDC (reports #US40181316 and #US47267621). 2021 through 2025 are estimates from IDC and do not reflect adjustments for inflation. Free-to-play game category includes microtransaction purchases and ad revenue.

The bottom line for investors: Focus on pricing power

I’m not ready to believe we are headed into a period of sustained inflation. But I do believe rising costs are likely to linger in the coming months, making it the biggest risk investors will face in 2022.

That’s why I am so focused on uncovering companies with pricing power.

I recently asked the investment analyst team that supports Washington Mutual Investors Fund to find examples of pricing power in the industries they cover. They came up with dozens of ideas, ranging from companies in the defense industry to technology and the consumer staples sector.

With slowing growth, rising inflation and other uncertainties on the horizon, 2022 may seem a daunting environment for investors. But I’m optimistic that an active portfolio of select companies with strong pricing power can help investors thrive in the years ahead.

Learn more about

Investing outside the United States involves risks, such as currency fluctuations, periods of illiquidity and price volatility, as more fully described in the prospectus. These risks may be heightened in connection with investments in developing countries.

MSCI World Index is a free float-adjusted market capitalization-weighted index that is designed to measure equity market results of developed markets. The index consists of more than 20 developed market country indexes, including the United States.

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.

Our latest insights

-

-

Economic Indicators

-

Demographics & Culture

-

Emerging Markets

-

RELATED INSIGHTS

Never miss an insight

The Capital Ideas newsletter delivers weekly insights straight to your inbox.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the mutual fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only. Use of this website and materials is also subject to approval by your home office.

Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.