Chart in Focus

Categories

Portfolio Construction

Constraints can be costly for investors — embrace flexibility

Clyde Bell

Clyde Bell

Sunder Ramkumar

Sunder Ramkumar

July 20, 2017

KEY TAKEAWAYS

- Flexible mandates can allow investment professionals to access their best ideas, helping skillful portfolio managers deliver better results.

- Several institutions, including Harvard University’s endowment, have been transitioning to broader investment mandates, based on the concern that style-based portfolios over-emphasize asset-class benchmarks at the expense of investor outcomes.

- A simulation model of large-cap stocks from 2002–2016 finds that flexibility to adjust the mix of value and growth companies would have increased average returns by up to 0.9% annually, depending on manager skill.

- A flexible investment universe may introduce short-term, benchmark-relative risk and drift, but can provide tools that objective-based funds need to achieve long-term goals.

- A case study of the American Funds family illustrates how the discipline of using flexibility to pursue objectives has resulted in measured changes in asset allocation and superior long-term results.

Style boxes have been used for many years to construct and monitor portfolios, but according to Casey Quirk (2013), several institutions are now beginning to move away from the model as too restrictive and, in some cases, not in the best interests of their organization or investors.

While style boxes can help bring structure to a portfolio, and style-based funds can easily be used to fulfill a desired asset allocation, such as large-cap growth or small-cap value, there is growing concern about adherence to such a relatively rigid process.

Officials at Harvard, for example, recently expressed concern about style boxes creating restrictive investment silos that could result in both gaps and duplication in a portfolio. In announcing a change in direction earlier this year, N.P. Narvekar, the CEO of Harvard Management Company, Inc., cited the “unintended consequences” of focusing on boxes. “This model has also created an overemphasis on individual asset-class benchmarks that I believe does not lead to the best investment thinking for a major endowment,” Narvekar said.

Harvard is part of a growing movement toward achieving greater investment flexibility by loosening constraints on the investment universe — and transitioning to broader investment mandates. In this article, we review theoretical and empirical evidence on the role of such investment flexibility.

Skill + investment opportunity = alpha

Although the issue is likely to be the topic of ongoing academic debate, significant research indicates managers constrained by style boxes underperform those with a broader mandate that allows them to invest in a more flexible manner.

For example, Howard and Callahan (2006) test four hypothetical trading strategies from 1995–2003 and find that limiting these strategies to fit in each of nine size/style boxes would have reduced annual alpha by an average of 339 basis points. Clarke et al. (2000) construct a more general Monte Carlo simulation to test a variety of constraints and also find that limits on size/style can hinder active results. In addition, Wermers (2002) finds that flexible funds have better results.

As an example of the potential benefits of flexibility, the chart below shows the universe of all U.S. large-cap value and growth stocks. Companies from both categories were combined and ranked by total return, and the top 50% of stocks in that list were apportioned to growth and value based on their Morningstar classifications. The data for the 15-year period ended December 31, 2016, illustrate two key insights:

First, while there are good companies in both value and growth styles every year, their proportion can vary significantly. Value companies made up 54% of the best performers in 2002, but only 19% in 2013.

Second, the stock selection opportunity was not just driven by macro regimes favoring value or growth. Value on average outpaced growth by 18% in 2002, yet almost half the best-performing stocks were growth. Similarly, in 2009, growth outpaced value by 33 percentage points, yet value stocks made up almost one-third of the best-performing companies.

Therefore, an investor who simply invested in the “winning” style every year — and ignored all the stocks in the “losing” style — would have missed opportunities.

It’s still about security selection

This example highlights how a bottom-up perspective provides unique insights, and that a flexible approach allows managers to tap into a broader opportunity set to navigate different market environments. For example, in the years depicted in the chart, an equal-weighted portfolio of the best companies every year would have outperformed one constrained to be balanced across value and growth stocks (i.e., in the same proportion as the overall market) by an average of 0.9% per year. This illustration focuses on the flexibility to adjust the mix of value and growth styles; the same principles apply to size, domicile and asset class flexibility.

Although flexibility expands the opportunity set, a broader investment universe alone is insufficient to generate superior results; the benefits of flexibility only accrue to the subset of fund managers who have stock-selection skill. For example, flexibility would not help a portfolio manager who is equally likely to pick an outperforming or underperforming stock. While flexibility is no silver bullet, it can serve to amplify the value of high-quality research.

Focus on objectives, not style boxes

These findings suggest that advisors should seek out portfolio managers with strong research capabilities and allow them to express investment conviction. The gains from flexibility may seem incremental, but can yield materially improved outcomes when compounded over typical investment horizons.

More importantly, these results prompt a critical evaluation of the broader role of investment constraints. Flexibility on size, style and domicile may introduce short-term, benchmark-relative risk and drift, but can provide tools that objective-based funds need to achieve long-term objectives. This approach has become more relevant as many advisors have embraced goals-based wealth management, in which success is defined increasingly as meeting long-term investor goals rather than simply outpacing market indexes.

Skillful investors could potentially benefit by combining looser constraints on the investment universe with a disciplined focus on investment objectives.

An investment strategy seeking long-term appreciation can often benefit from investing in companies with low valuation, as these might represent turn-around opportunities. Similarly, an investment strategy seeking current income may benefit from diversification across dividend-paying companies and high-yielding fixed income. In these scenarios flexibility can provide avenues for improved results, as well as greater diversification.

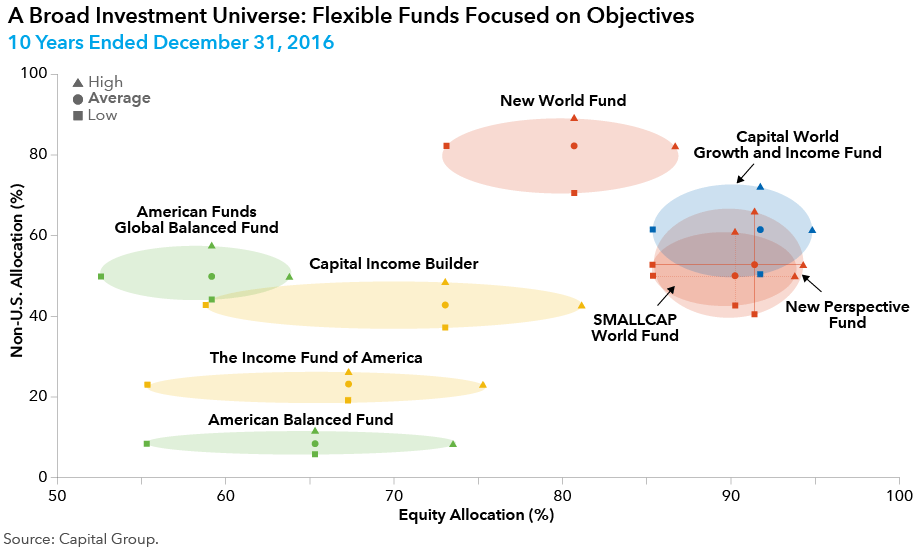

Funds in the American Funds family with global equity and multi-asset mandates form an interesting case example. These use a broad investment universe to pursue a range of objectives including appreciation, growth and income, income, preservation and even a balance of multiple objectives.

The disciplined focus on investment objectives has resulted in measured changes to asset allocation, as illustrated in the chart below.

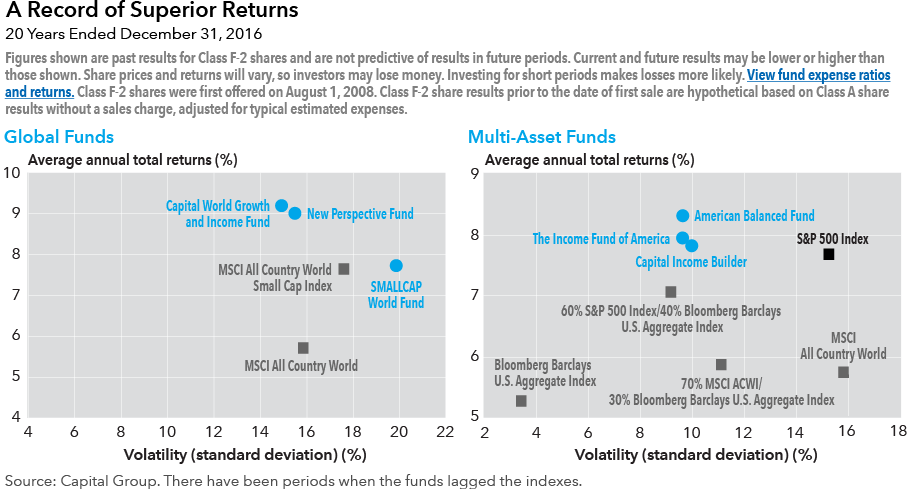

Although past results are not predictive of future returns, these flexible funds with at least a 20-year history have demonstrated superior long-term returns, often with lower volatility than index benchmarks. The data suggest that the benefits of including such funds outweigh the modest adjustments that advisors might have to make to their portfolio construction practice.

Learn more about

Works cited

Clarke, Roger; Harindra de Silva; and Steven Thorley. “Portfolio Constraints and the Fundamental Law of Active Management.” Financial Analysts Journal, vol. 58, no. 5, September/October 2002, pp 48-66.

Howard, C. Thomas and Craig T. Callahan. “The Problematic ‘Style’ Grid,” Journal of Investment Consulting, vol. 7, No. 3, Winter 2005-06, pp 48-60.

Wermers, Russ (2002). “A matter of style.” Canadian Investment Review. Summer, vol. 42.

Investment results assume all distributions are reinvested and reflect applicable fees and expenses.

Investing outside the United States involves risks, such as currency fluctuations, periods of illiquidity and price volatility, as more fully described in the prospectus. These risks may be heightened in connection with investments in developing countries.

MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.

The S&P 500 is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2017 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC.

© 2017 Morningstar, Inc. All rights reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

Bloomberg Barclays indexes are unmanaged, and results include reinvested dividends and/or distributions but do not reflect the effect of sales charges, commissions, account fees, expenses or U.S. federal income taxes.

S&P 500 Index is a market-capitalization-weighted index based on the results of 500 widely held common stocks. This index is unmanaged, and its results include reinvested dividends and/or distributions but do not reflect the effect of sales charges, commissions, account fees, expenses or U.S. federal income taxes.

Bloomberg Barclays U.S. Aggregate Index represents the U.S. investment-grade fixed-rate bond market.

MSCI indexes are free-float-adjusted, market-capitalization weighted indexes. Developed market index results reflect dividends net of withholding taxes. Emerging market index results reflect dividends gross of withholding taxes through December 31, 2000, and dividends net of withholding taxes thereafter. Each index is unmanaged, and its results include reinvested dividends and/or distributions but do not reflect the effect of sales charges, commissions, account fees, expenses or U.S. federal income taxes.

MSCI All Country World Index (ACWI) is designed to measure results of more than 40 developed and emerging equity markets.

MSCI All Country World Small Cap Index is a free float-adjusted market capitalization weighted index that is designed to measure results of smaller capitalization companies in both developed and emerging equity markets.

Past results are not predictive of results in future periods.

Our latest insights

-

-

Economic Indicators

-

Demographics & Culture

-

Emerging Markets

-

RELATED INSIGHTS

-

Portfolio Construction

-

Portfolio Construction

-

Portfolio Construction

Never miss an insight

The Capital Ideas newsletter delivers weekly insights straight to your inbox.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the mutual fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only. Use of this website and materials is also subject to approval by your home office.

Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.