We may one day remember the pandemic as a turning point for women and money. In a year of so much change, 2020 was marked not only by economic crisis, but also by a renewed quest for financial resilience and security.

In Women’s financial futures: New financial philosophies taking shape post COVID-19, Capital Group’s latest Wisdom of Experience investor survey of approximately 2,000 women and 500 men, we found that COVID had an outsized financial impact on women, particularly millennials and women of color. Since the early phase of the pandemic, women have been more likely than men to lose their jobs — and, many months later, to still be out of work.

“Women of color and millennial women are more likely to have known someone who experienced a job loss or financial hardship,” says Lorna Fitzgerald, senior market researcher at Capital Group,

Women are also more likely to be concerned about money, to let money worries affect their personal wellbeing, and to stop retirement plan contributions and take early withdrawals from qualified retirement accounts. In short, they are an investor base in need of financial advice from a qualified professional.

This presents several opportunities:

- Women represent a demographic with growing buying power and investable assets.

- They can be influencers among other powerful clients.

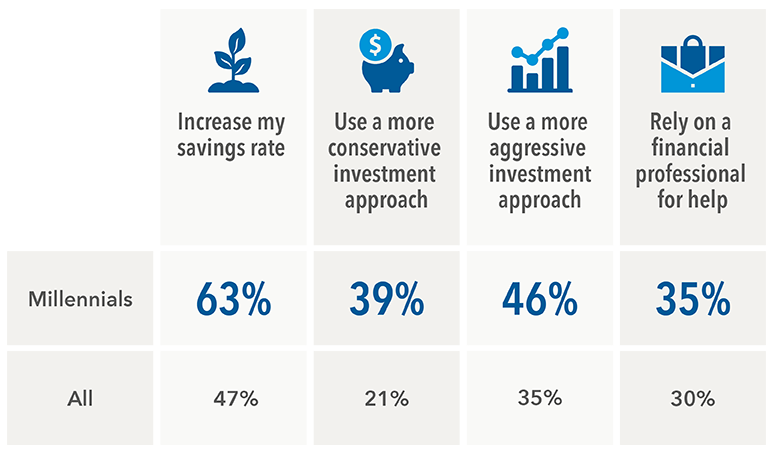

- Our findings indicate that many women view the pandemic experience as an opportunity to take control of their finances and build more resilient futures.

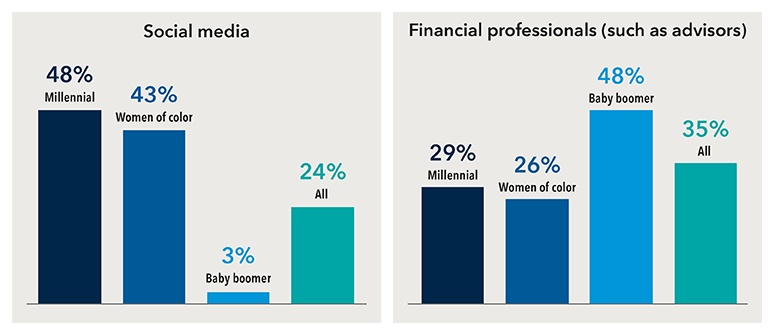

- Where women turn for financial advice differed greatly depending on age, wealth, race and other factors.

Financial professionals who are interested in serving these markets should be aware: Most of them won’t be found through the industry’s typical channels or approaches to client acquisition. To engage these women, you have to understand who they are, and where and how they seek advice. Here are four tips to help win women clients now.