Chart in Focus

Categories

United States

10 charts that explain what you need to know about the U.S. economy

The U.S. economy has been through a lot in the last decade. Since the financial crisis, economic growth has been slow but consistent, while stocks have surged. But the big question on everyone’s mind is, “Is this sustainable?” We think so. Here’s why.

The current expansion is one of the longest in U.S. history – but is it reaching its end?

The U.S. expansion is now entering its eighth year, which is long by historical standards, and has led some investors to ask whether it is on its last legs. While the expansion is indeed longer than most, there is precedent for it to continue, including a 10-year run starting in 1991. Elsewhere in the world, some countries have even enjoyed multi-decade expansions.

Expansions don’t simply die of old age, but rather from excesses or imbalances in an economy, which is not the case with the United States’ gradual but steady economic expansion.

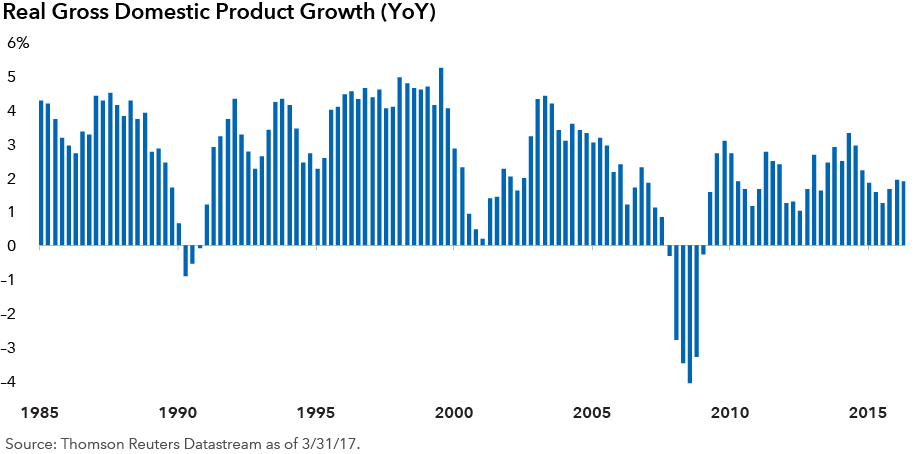

Since the last recession, gross domestic product has averaged 2.1% annual growth, far lower than the 4.4% it averaged over the previous 10 recoveries. While growth has been sluggish at times, it has allowed the expansion to persist longer than average and potentially gives it more room to run.

So where is the economy now?

An important factor in the economy’s slow expansion has been weaker industrial activity, which has acted as a drag even as consumer spending has been strong.

Sluggish global growth has been a headwind for industrials, but manufacturing has shown improvement in recent months throughout the world. Higher infrastructure spending under the new administration could potentially boost growth even further.

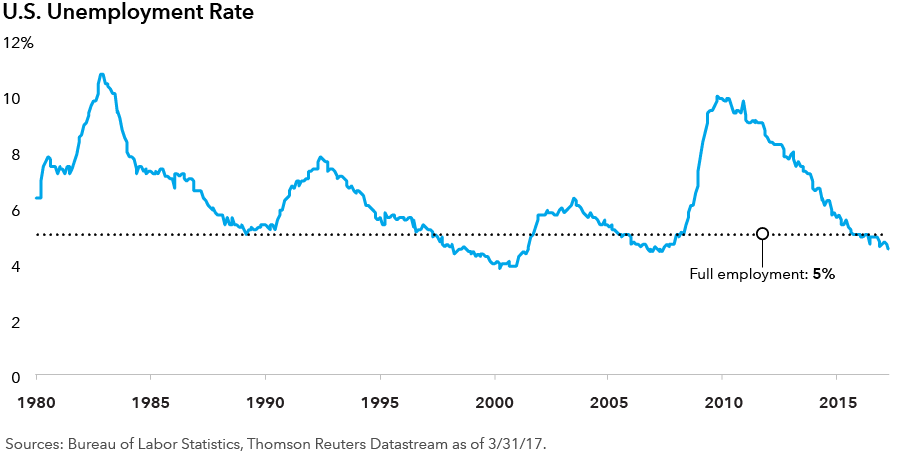

A strong labor market has bolstered consumer spending. The unemployment rate has steadily improved since the financial crisis and is currently below 5%, often characterized as full employment.

Wage growth was stagnant for much of the recovery, but has accelerated over the past year. Higher wage growth is helping boost inflation expectations, which is now near the Federal Reserve’s 2% target.

What does this mean for my investments?

While economic growth has been slow, there has been nothing sluggish about U.S. equity returns. The S&P 500 is up over 280% since the financial crisis, easily outpacing its global peers.

The market has rewarded those who stayed invested in the face of significant global uncertainty. Events such as the European debt crisis, plunging oil prices, a slowdown in China and the Brexit decision threatened to derail the bull run, but U.S. stocks continued to be resilient.

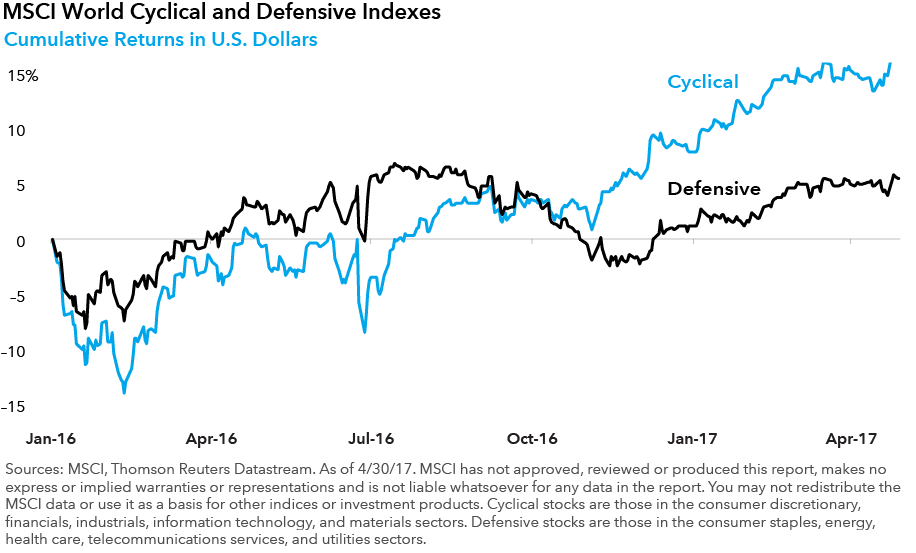

While all areas of the market have been rising, cyclical stocks have outpaced defensive stocks in recent months following the U.S. presidential election. Expectations of a tax cut and increased infrastructure spending have boosted investor sentiment.

Financial stocks have done exceptionally well during this time on the prospects of higher interest rates and a rollback of some regulations.

The powerful bull market of the last eight years has lifted valuations above historical averages. Nevertheless, there are still bargains to be found in companies, but the current environment requires extensive research and selective investments.

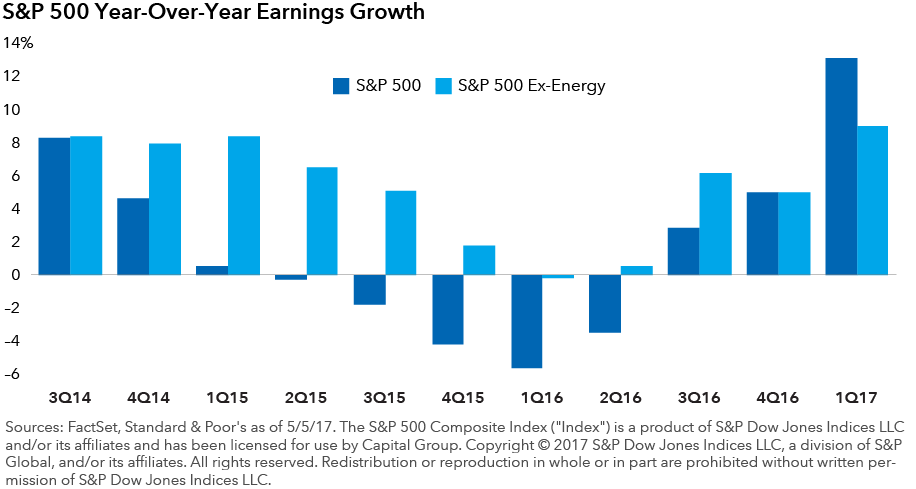

The good news for companies is that they are making money again. Early in 2016, negative earnings growth sparked recession talk, but corporate profits have improved amid a rebound in energy prices and more optimistic views of the global economy. Earnings grew 13.5% in the first quarter of 2017, the fastest pace since 2011, according to data aggregator FactSet. Continued higher earnings growth would help stocks grow into their current lofty valuations.

What else should U.S. investors watch for this year?

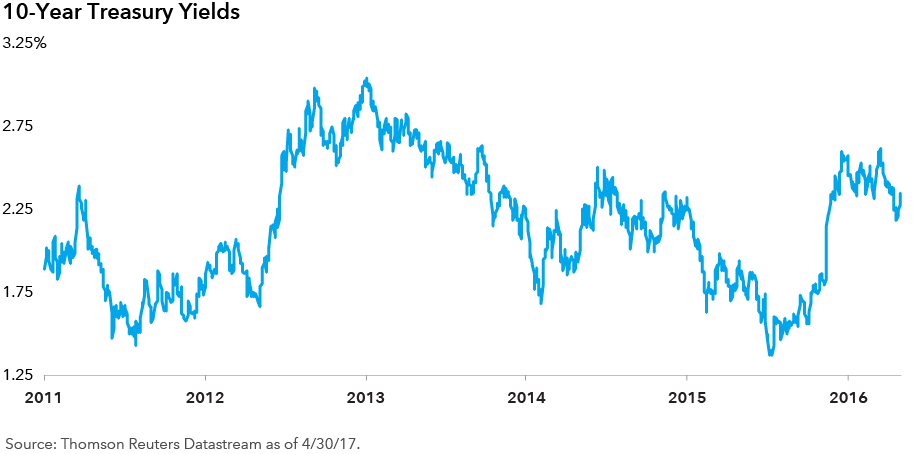

The Federal Reserve will have investors’ attention throughout the year. After raising interest rates in December, they signaled three more hikes in 2017. The Fed already increased rates at its March meeting, and higher inflation and economic growth would support additional hikes.

But despite higher policy rates, don’t expect yields to rise rapidly. Low sovereign bond yields and accommodative central banks elsewhere in the world could anchor U.S. rates.

Investors should also keep an eye on currency markets. The U.S. dollar has risen dramatically since 2011, but signs are pointing toward a plateau or even a modest decline this year.

A weakening dollar would provide a tailwind to domestic exporters, and also benefit international investment returns for U.S.-based investors.

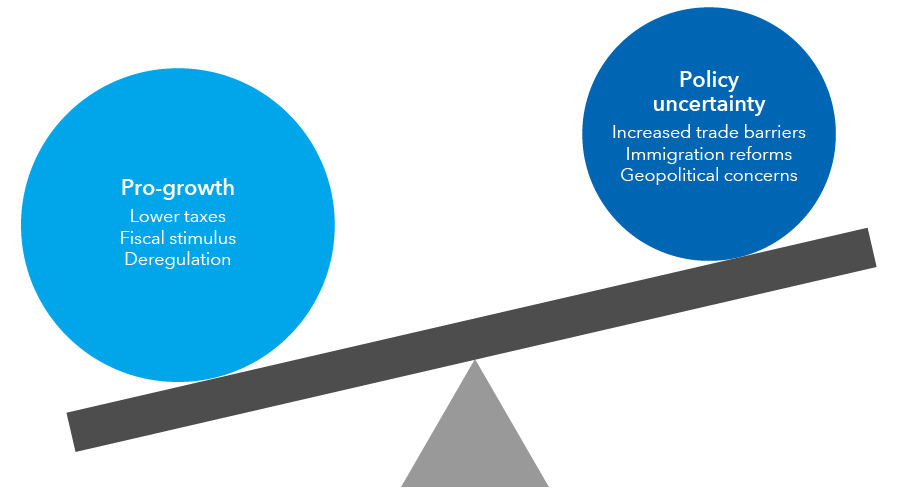

Finally, the new presidential administration’s ability to fulfill campaign promises will be critical. Higher infrastructure spending, tax reform, and financial deregulation would boost growth if they come to fruition, but could partially be offset by uncertainty over trade barriers and new immigration restrictions.

Learn more about

Past results are not predictive of results in future periods.

Investing outside the United States involves risks, such as currency fluctuations, periods of illiquidity and price volatility, as more fully described in the prospectus. These risks may be heightened in connection with investments in developing countries.

Our latest insights

-

-

Economic Indicators

-

Demographics & Culture

-

Emerging Markets

-

Related Insights

-

Economic Indicators

-

Chart in Focus

-

Economic Indicators

Never miss an insight

The Capital Ideas newsletter delivers weekly insights straight to your inbox.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the mutual fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only. Use of this website and materials is also subject to approval by your home office.

Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.