Chart in Focus

Categories

Dividends

Where in the world are the dividends? Try going global

Jim Lovelace

Jim Lovelace

September 18, 2018

KEY TAKEAWAYS

- U.S. investors seeking dividend income face certain challenges in today’s market.

- Rising rates, stretched valuations and relatively modest yields present risks for dividend-focused investors.

- Global markets have become fertile hunting grounds for higher-yielding stocks.

Lately, dividend investors have faced some tough sledding. Growth-oriented companies have been leading the bull market for what seems like an eternity. Yet valuations for some dividend payers in perceived safe havens of the market are elevated by historical standards. With interest rates rising, income investors may be wondering where they should turn to find dividend opportunities. Part of the answer, according to Jim Lovelace, principal investment officer and portfolio manager for Capital Income Builder®, is going global. Jim recently sat down with us to share his perspective on six key questions facing dividend investors today.

Capital Income Builder is a globally diversified equity-income fund that focuses on generating a growing stream of income that exceeds the yield paid by U.S. companies in general.

Can dividend-oriented income investors stay focused on U.S. markets, or has it become essential to take a global approach?

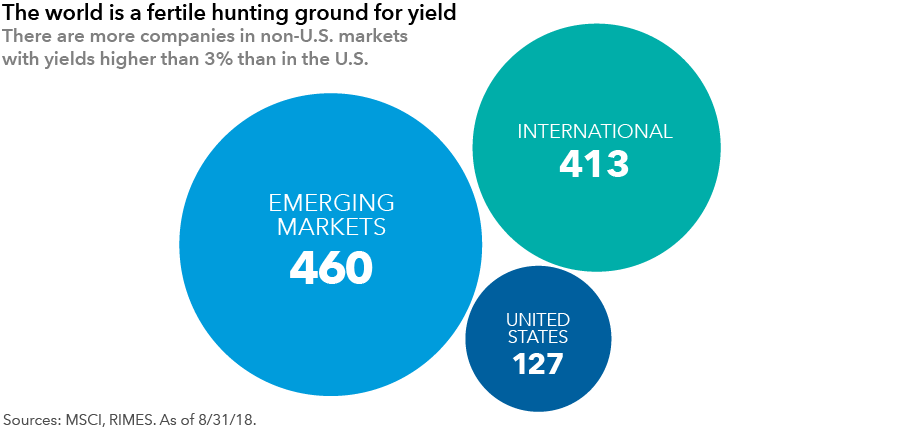

For an income portfolio, it's a lot easier to find opportunities when taking a global approach. The U.S. market since the tech bubble of the late '90s and the early 2000s has been one of the lower-yielding markets in the world. Today, the yield on the S&P 500 is a little less than 2%. Whereas the yield of the rest of the developed markets, using MSCI EAFE as a point of reference, is a little over 3%. So that tells you there are more yield opportunities outside the U.S. than inside the U.S.

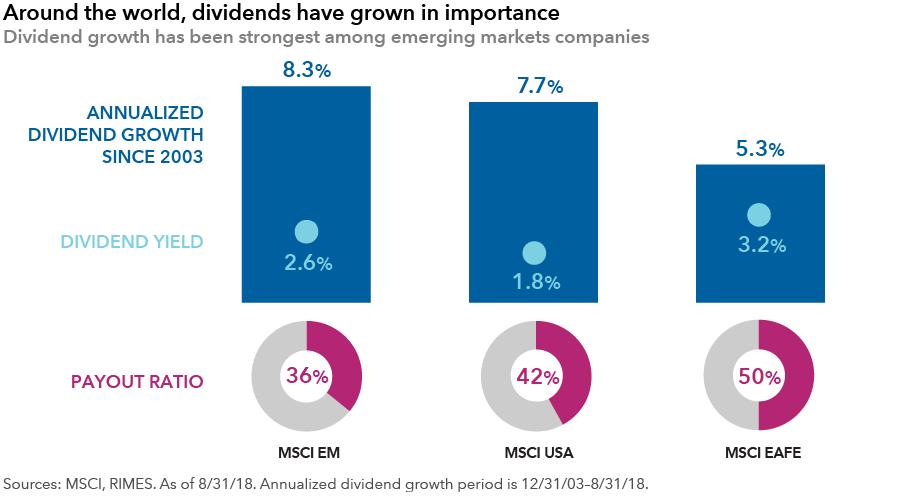

When you go back to the 1980s, few markets were oriented toward dividends. Besides the United States, there was the United Kingdom, Australia, Hong Kong, Canada — and those were the primary markets. Over the years, companies domiciled in many countries have learned the value of having companies distribute dividends to investors. Dividends help to stabilize markets and help contribute to companies' total returns over long periods.

So now Continental Europe is one of the best markets for finding good dividend growth investments. Southeast Asia beyond Hong Kong is a very fertile market for companies that have a healthy dividend culture and strong growth. So the opportunities have really grown. As a case in point, about half of Capital Income Builder’s equity investments are in non-U.S. securities. Part of it is the relative valuation – non-U.S. markets today are much cheaper than U.S. markets. Nevertheless, it gives you a sense of the extent to which we look to international markets for meeting income objectives.

But should investors be concerned that a strengthening U.S. dollar could erode the value of their dividends from non-U.S. markets?

All companies pay their dividends out of their earnings. Whether they are paying out a strict percentage of their earnings or approximating that with a dividend policy, we have to start with the question of how stable are the cash flows that underpin the dividend? That's the essence of dividend investing. If you make an investment and the cash flows are not stable, that's when you experience a reduction in income. So the fundamental analysis as to whether a company can support the dividend always remains much more important and outweighs other factors.

Of course, we also have to factor in currency risk. Ultimately, the standard for an investment is growth of income for a U.S. dollar-based investor. If there is a risk that the currency will diminish or eliminate the dividend growth, that's not an attractive investment.

Will dividend-oriented stocks continue to lag growth stocks?

I try not to be drawn into a horse race with growth stocks. My goal in leading a strategy like Capital Income Builder is to provide an investment program that provides the potential for stable equity-like investment returns over a long period. Our primary focus is the absolute return. When times get tough and the market goes down, are we holding onto the value and not going down with the markets? That’s particularly important when you get into a late cycle period like the one we’re in today.

Do rising interest rates still matter to dividend-paying stocks?

Well, stocks overall are not necessarily always hurt by rising interest rates. It’s important to understand that the main driver for rising interest rates is strong economic activity. And that can be helpful to corporate profits. So in the early to mid-stages of an expansion, you'll see rising interest rates and rising stock prices.

It's only toward the end of a cycle, when their excess is beginning to build up and the Federal Reserve is trying to slow things down, that interest rates can have a negative impact on stock prices.

As interest rates are now coming back up to historically “normal” levels, we're seeing the overall income flow growing again. So I think that rising interest rates will help the growth of the income element of Capital Income Builder.

In what areas of the market are you finding opportunity?

We find value in most areas of the market, but they're very specific situations. Almost every industry has its higher-yielding companies, and they're higher yielding for different reasons. Some are mature businesses that have chosen to reward investors with excess cash flows. Others might be turnaround companies deemed risky by the market.

Some sectors typically associated with high-yield — utilities, telecommunications, tobacco, energy and financials — tend to be interest-rate sensitive. So we do try very hard to find opportunities in some of the other industries to diversify away from that interest-rate sensitivity. Investments in technology stocks like Microsoft and companies in the health sector like Abbvie or Amgen, all three among the fund's 10 largest holdings,1 have emerged as important areas of the market where investors can obtain dividend income and growth of income, and without the interest rate sensitivity of traditional dividend-paying stocks.

Every investment we make is evaluated on its current income and its growth potential relative to the objective of the fund: to provide an above-average yield, say 3.5%, and growth of income. Our investment analysts generate proprietary estimates of dividend growth over three years for each of the companies they cover. We plot those estimates, as well as the company’s current dividend yield, along a curve. That helps us determine whether a company is a good investment for the fund. If a stock yields substantially more than that 3.5% then maybe we don't expect any growth, or 1 to 2% would be sufficient. But if it yields 3.5%, we would expect it to grow 5%. And if it yields less than 3.5%, we'd expect it to grow 10 or 15%. So that is what makes up the portfolio: stocks on that spectrum.

How important are economic cycles to dividend-paying stocks? Where are we in the current cycle?

I'm not sure it's useful to talk about economic cycles, because the economy isn't cycling the way it used to. There was a well-defined economic cycle in the U.S. into the 1980s. But starting in the 1990s, the cycle has become less and less pronounced. A lot of that has to do with the fact that manufacturing as a percent of the overall economy has diminished. It's less than 10% of employment in the U.S.

One of the key drivers of the economic cycle was inventory cycles. Starting in the 1980s, just-in-time inventory management changed the nature of the cycle dramatically. The growth of the service sector and technology also accentuated that. What we see today are different industries having their own cycles to whatever their key driver is. We still have recessions from time to time, but the last couple have been driven more by financial matters than manufacturing issues. And those will happen when there is some excess that needs to be corrected for. But that's not a cycle, that's a reaction.

1 As of 7/31/18, AbbVie comprised 2.8%, Microsoft 1.5% and Amgen 1.4%, respectively, of Capital Income Builder net assets.

Learn more about

Investing outside the United States involves risks, such as currency fluctuations, periods of illiquidity and price volatility, as more fully described in the prospectus. These risks may be heightened in connection with investments in developing countries.

The return of principal for bond funds and for funds with significant underlying bond holdings is not guaranteed. Fund shares are subject to the same interest rate, inflation and credit risks associated with the underlying bond holdings.

Our latest insights

-

-

Economic Indicators

-

Demographics & Culture

-

Emerging Markets

-

RELATED INSIGHTS

-

Dividends

-

-

Asset Allocation

Never miss an insight

The Capital Ideas newsletter delivers weekly insights straight to your inbox.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the mutual fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only. Use of this website and materials is also subject to approval by your home office.

Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.