Chart in Focus

Categories

Fixed Income

Fixed income outlook: Meet uncertainty with balance

Pramod Atluri

Pramod Atluri

Mike Gitlin

Mike Gitlin

Margaret Steinbach

Margaret Steinbach

December 10, 2019

KEY TAKEAWAYS

- Trade tensions and a slowing Chinese economy are hampering global growth.

- We expect central banks to remain accommodative and rates to remain lower for even longer.

- Credit is expensive and susceptible to equity volatility.

- A strong core bond allocation can help provide stability.

- Municipal bonds and emerging markets debt offer attractive relative value.

The Federal Reserve this week confirmed market expectations that rate cuts are on pause for now. Among developed markets, the U.S. has become the exception in a world where negative rates are the strange new normal. Yet, negative yielding bonds are just one of the many odd consequences of aggressive monetary policy.

Imagine walking into a bank to open a savings account and learning that the bank will charge you interest on your deposits. That’s exactly what UBS is doing in Europe for balances exceeding 500,000 euros.

Imagine buying a home and your mortgage broker telling you that you can borrow more than you have to pay back. Borrowers in Demark are living this dream thanks to negative mortgage interest rates.

Just how negative have bond yields become? Swiss government bond yields are negative all the way out to 50-year maturities. A whopping 20% of European investment-grade corporate bonds are negative-yielding.

“In an extraordinary market like this, balance is essential,” says Mike Gitlin, head of fixed income at Capital Group. “Amid unusual market trends and mixed economic indicators, a strong core bond allocation is your best defense. It can help to absorb unexpected volatility in equity markets.”

Macro: The only certainty is uncertainty

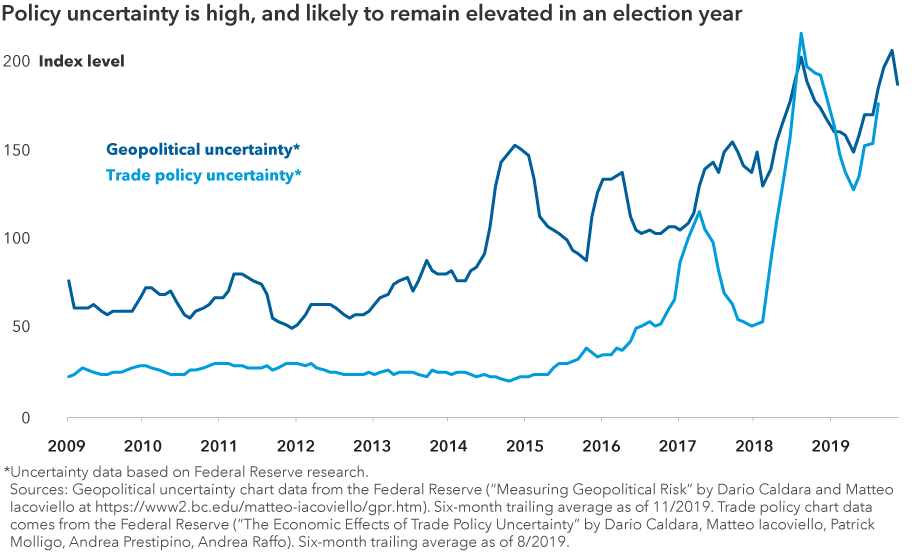

“2019 saw both equity and fixed income markets generate remarkably strong returns for investors,” explains Pramod Atluri, portfolio manager for The Bond Fund of America®. “Such strong returns for both asset classes are unusual given the backdrop of weaker global economic growth, lower earnings growth, elevated geopolitical uncertainty and trade tensions.”

Perhaps the biggest threat to global growth is China’s slowing economy. While ongoing trade policy jolts have contributed to some of the country’s troubles, other issues also plague its economy. Credit growth has weakened, unemployment is rising and wage growth is falling for lower skilled workers. Although the Chinese government’s official GDP growth estimate is 6% for the year, Capital Group economists think it could be weaker. If the world’s second largest economy continues to stumble, the domino effect on other countries could be significant. Those that export goods to China will see slowing demand. Global commodity producers will also suffer with Chinese businesses requiring fewer resources than expected.

Outside of China, the broader global outlook is not bright. Europe and Japan are both struggling with lackluster GDP growth around 1%. Economic indicators on both the business and consumer sides have seen downward trends since 2017.

Are prospects better in the U.S.? “Unemployment is hovering at the lowest levels in 50 years, and wage growth is finally picking up at around 3%. Consumer confidence is also relatively strong,” Gitlin says.

“But that’s only half the story,” he continues. “Businesses look more bearish. Profit margins are declining as companies deal with those rising wages and higher costs of commerce due to tariffs. Manufacturing activity has contracted for four straight months, with fewer new orders and slower production. The U.S. has become a tale of two economies. Either the consumer will continue to carry growth or bearish businesses will push the U.S. toward recession.”

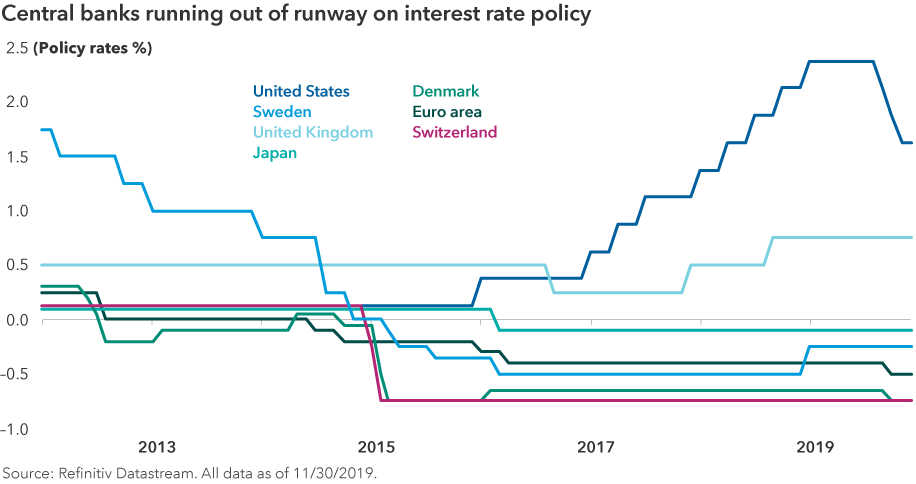

Given heightened policy uncertainty and slower growth, central bankers are unlikely to reverse course on their stimulus measures anytime soon. U.S. interest rates, which were thought to be on an upward trend as recently as late 2018, have declined. They are now expected to remain lower for even longer.

“The Federal Reserve’s own estimates indicate that its policy rate isn’t likely to exceed 2.5% through at least 2022,” says Margaret Steinbach, a fixed income investment director at Capital Group. “Bond investors see yields remaining very low for years to come — futures markets predict the 10-year Treasury yield to stay below 2.25% through 2024.”

Policy rates are near or below zero in most developed markets. Central bank balance sheets never shrank meaningfully and remain bloated post-crisis. That leaves monetary policymakers with less ammo to battle the next downturn.

“If central banks can’t resuscitate global growth, it may be fiscal policy’s turn to lend a hand,” Gitlin says. Fed Chair Jerome Powell suggested this last month. He urged U.S. lawmakers to get the nation’s finances in order so that the federal budget will have more leeway to provide stimulus when needed. Central bankers in other developed economies have made similar pleas for fiscal measures to pick up the slack. In fact, earlier this month Japan announced a new fiscal stimulus.

Markets: Inflated asset prices pose downside risk

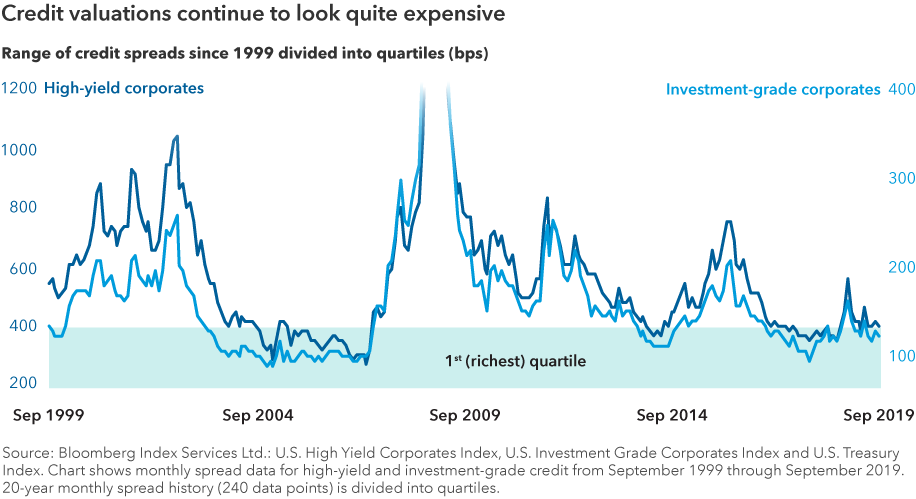

Asset prices have been perhaps the biggest beneficiary of aggressive monetary policy intervention. Equity markets have flourished in recent years. But that’s just one example. Bonds, real estate and most major asset classes are at the high end of their 15-year valuation range.

Credit has become expensive relative to history and given the macro risks. In late 2019, credit spreads for both investment-grade and high-yield corporate bonds were hovering within or just above their richest quartile over the past 20 years.

When within this richest quartile, investors have historically earned an annualized 200 to 300 basis points more owning Treasuries instead of credit in the two years that followed. “We should expect to see more modest returns for investment-grade and high-yield bonds in 2020 than what we saw in 2019,” Atluri explains.

Investor solutions: How to keep your balance in a wobbly world

1. Look to core for balance

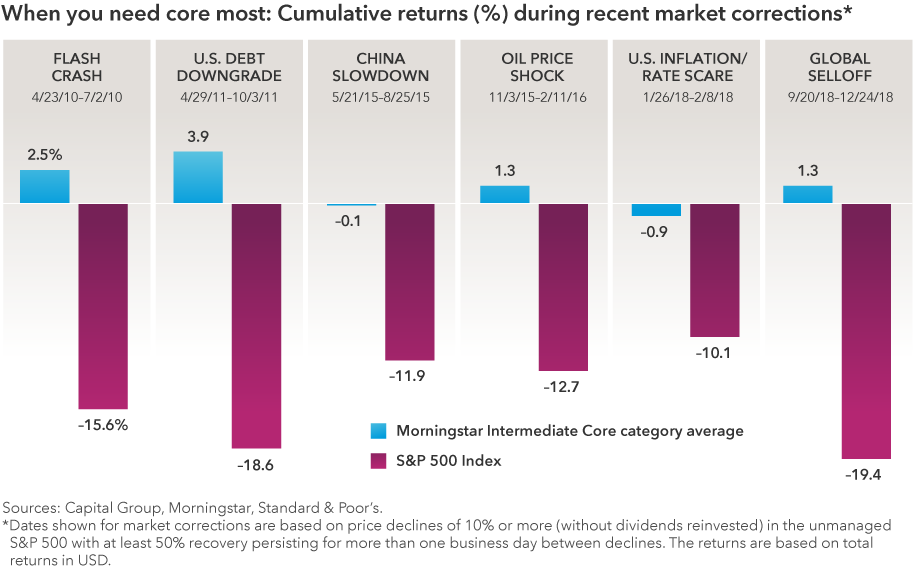

“The best way to balance a portfolio in uncertain times is to build a strong core bond allocation,” Gitlin says. “What does that mean? It means holding bonds that will provide not only income, but the other roles of fixed income as well: diversification from equities, capital preservation and inflation protection. That way, no matter what the market environment, fixed income should help portfolio resilience through the balance it can provide.”

Consider what happened during the six equity correction periods of 10% or more since 2010. In each of these periods, core taxable and tax-exempt funds persevered.

“Of course, some investors may need more tailored fixed income options that go beyond a core bond allocation to stress one role of bonds more than the other three,” he adds. “In those cases, more targeted strategies can be sprinkled in.”

A government securities fund can help if looking for more diversification from equities. An inflation-linked bond fund might be a good addition if looking for more inflation protection. Stressing ultra-high-quality, shorter term bond funds can help to better preserve capital.

However, when addressing such specific investor needs, a portfolio should remain reasonably balanced. A strong core fixed income foundation that includes a true core bond fund, like The Bond Fund of America, should help investors achieve that balance.

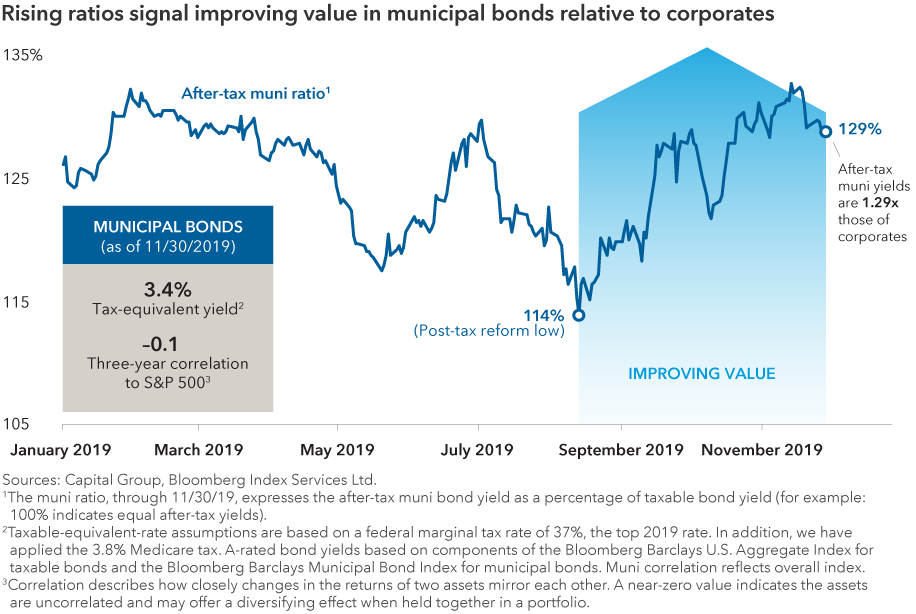

2. Got taxes? Get munis

Municipal bonds can play many of the same roles as taxable bonds. But they come with an added benefit of higher after-tax income.

Investors in the highest tax brackets historically have piled into munis; however, they are also a relatively attractive source of after-tax income for investors in other brackets. Despite muni yields near multiyear lows, after-tax yields have continued to exceed those of taxable bonds for anyone whose marginal tax rate is 24% or higher — well below the top tax rate of 37%. Furthermore, munis’ relative value compared to like-rated corporates has risen in the second half of 2019.

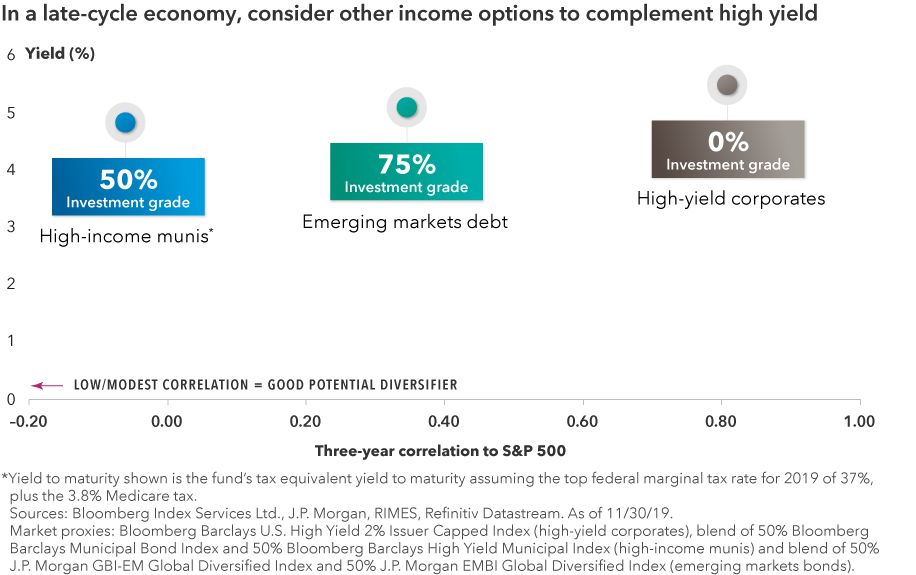

3. Consider complements to high yield

High-yield corporate bonds have recently been a go-to source for investors looking for more income. However, as the sector has seen strong inflows and loftier valuations, its returns are likely to moderate. Credit spreads are tight in this late phase of the economic cycle. In this environment, high-yield bonds are asymmetrically susceptible to losses, suggesting those looking for enhanced income should think more broadly.

On the taxable side, emerging markets debt has provided similar levels of income but a lower correlation to equities. That means its returns or losses have historically not been as closely linked to those of stocks.

For investors, the trade-off here comes in the shape of greater potential volatility due to currency and interest rate movements. And — as underscored by Argentina’s recent change of government — political, fiscal and monetary policies can move quickly. However, this episode also demonstrates that emerging markets are idiosyncratic, as Argentina's problems were largely isolated. The sector offers a wide array of investment opportunities. One country’s troubles won’t necessarily lead to contagion for the entire sector. A research-driven approach focusing on country fundamentals is, therefore, crucial.

“Through prudent investing, emerging markets debt, in our view, offers a relatively high level of compensation for the risks entailed,” Steinbach says.

On the tax-exempt side, high-income municipals hold a special distinction. They have provided a similar level of after-tax income as high-yield corporates, but with no correlation to equities. Once again, research matters here, as risk is higher in this sector. But understanding issuer fundamentals can help to identify better opportunities.

Investors should look for balance and rely on fixed income to provide balance. A strong core bond allocation that provides all four roles of fixed income can help investors achieve better long-term outcomes.

Learn more about

The return of principal for bond funds and for funds with significant underlying bond holdings is not guaranteed. Fund shares are subject to the same interest rate, inflation and credit risks associated with the underlying bond holdings. Lower rated bonds are subject to greater fluctuations in value and risk of loss of income and principal than higher rated bonds. Income from municipal bonds may be subject to state or local income taxes and/or the federal alternative minimum tax. Certain other income, as well as capital gain distributions, may be taxable. While not directly correlated to changes in interest rates, the values of inflation-linked bonds generally fluctuate in response to changes in real interest rates and may experience greater losses than other debt securities with similar durations. Bond ratings, which typically range from AAA/Aaa (highest) to D (lowest), are assigned by credit rating agencies such as Standard & Poor's, Moody's and/or Fitch, as an indication of an issuer's creditworthiness. If agency ratings differ, the security will be considered to have received the highest of those ratings, consistent with the fund's investment policies. Investing outside the United States involves risks, such as currency fluctuations, periods of illiquidity and price volatility, as more fully described in the prospectus. These risks may be heightened in connection with investments in developing countries.

©2019 Morningstar, Inc. All rights reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

Bloomberg® is a trademark of Bloomberg Finance L.P. (collectively with its affiliates, “Bloomberg”). Barclays® is a trademark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Neither Bloomberg nor Barclays approves or endorses this material, guarantees the accuracy or completeness of any information herein and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Standard & Poor’s 500 Composite Index is a market capitalization-weighted index based on the results of approximately 500 widely held common stocks. This index is unmanaged, and its results include reinvested dividends and/or distributions but do not reflect the effect of sales charges, commissions, account fees, expenses or U.S. federal income taxes. Investors cannot invest directly in an index. Standard & Poor’s 500 Composite Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2019 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part is prohibited without written permission of S&P Dow Jones Indices LLC.

Our latest insights

-

-

Economic Indicators

-

Demographics & Culture

-

Emerging Markets

-

Related Insights

-

Asset Allocation

-

Dividends

-

Never miss an insight

The Capital Ideas newsletter delivers weekly insights straight to your inbox.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the mutual fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only. Use of this website and materials is also subject to approval by your home office.

Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.