Chart in Focus

Categories

Trade

Will a trade war push the U.S. economy into recession?

Darrell Spence

Darrell Spence

Jared Franz

Jared Franz

August 13, 2019

KEY TAKEAWAYS

- The U.S. economy looks healthy based on underlying fundamentals.

- It’s a tale of two economies: strong domestic demand but weaker industrial activity.

- Federal Reserve rate cuts should provide a tailwind for stocks.

- A brewing trade war with China remains the biggest wild card.

If you’re just returning from a few weeks of summer vacation, then welcome back to a fundamentally changed investment environment. Since July 31, the Federal Reserve has cut interest rates for the first time in a decade, the U.S.-China trade dispute has intensified and market volatility has returned with a vengeance.

Against this backdrop, Capital Group economists Darrell Spence and Jared Franz have revisited their outlook for the U.S. economy, including the prospects for a near-term recession. In the following Q&A, they offer their thoughts on the Fed’s dramatic policy shift, the potential impact of new tariffs on China and what it all means for investors.

How have these events influenced your assessment of the U.S. economy?

Darrell Spence: In many ways, the U.S. economy still looks fundamentally healthy. GDP growth is averaging above 2% on an annualized basis. Retail sales are solid. Wages are rising in excess of inflation. Job growth is strong and the unemployment rate is well below 4%. If we just look at the domestic data, the U.S. economy remains in good shape.

Given these domestic conditions, our base case is that the decade-long U.S. economic expansion isn’t immediately threatened by China trade tensions or slowing economic growth elsewhere in the world. However, any further deterioration in the trade environment would, in our view, substantially raise the risk of a U.S. recession.

With the U.S. imposing new tariffs on China later this year and China moving to devalue its currency, the situation is clearly getting worse. It’s hard to know where the tipping point lies.

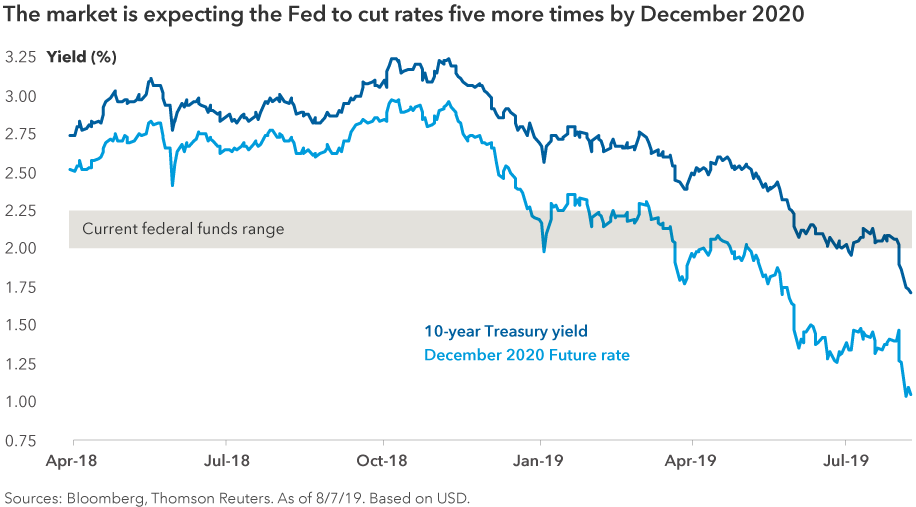

Are falling bond yields and an inverted yield curve predicting a recession?

Jared Franz: One of the many reasons that bond yields have fallen so precipitously is that the market believes the Fed will reduce rates an additional five times between now and year-end 2020, assuming cuts of 25 basis points each. Including the July move, that would be 150 basis points over an 18-month period, a pace that has occurred only once outside of a recession. An inverted yield curve — where short-term rates exceed long-term rates — is sending the same signal.

That said, there are other factors pushing U.S. bond yields lower, including negative interest rates in Europe and Japan. Bonds trade in a global market, and it could be that investors are not satisfied with 10-year German bunds yielding around –0.6%. In that environment, U.S. Treasuries at 1.6% obviously look a lot more attractive.

With the European Central Bank likely to cut policy rates further into negative territory next month, global bond yields are effectively acting as an anchor on U.S. yields. That may help to explain why the bond market appears to be predicting a recession while U.S. stocks remain near all-time highs.

Are there any signs of weakness in the domestic economy?

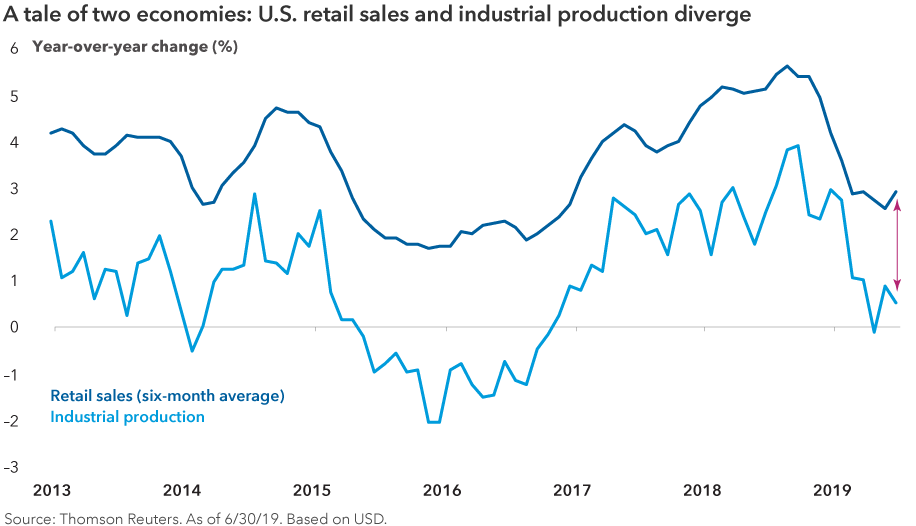

Spence: We see a tale of two economies: strong domestic consumption but weaker industrial activity. Declining exports and pre-tariff inventory stocking are undoubtedly playing a role as the precarious trade environment weighs on industrial production. At the same time, the consumption side looks strong, and we’ve seen a decent bounce back in U.S. retail sales. This is not unlike the economic environment we experienced in 2015–16.

The gap between industrial production and retail sales, in our view, will eventually narrow through a recovery in industrial activity rather than slowing domestic demand. Exports only account for about 13.2% of U.S. output, so domestic factors tend to drive the overall direction of the economy.

Again, though, this optimistic view is based on an assumption that the U.S. and China are able to avoid a full-blown trade war. If the U.S. imposes 25% tariffs on all Chinese imports, for instance, and China retaliates, then that would present a very difficult scenario that would almost guarantee recessionary conditions in the U.S. and globally.

Do you think the Fed would ever resort to negative interest rates?

Franz: I don’t think so. Negative interest rates are incredibly damaging to the banking sector, as we’ve seen in Europe and Japan. They also make it very difficult for central banks to respond if economic conditions deteriorate further. The Fed would likely use quantitative easing, forward guidance and other tools first, and only consider a negative-rate policy in the event of another global financial crisis on the scale of 2008–09.

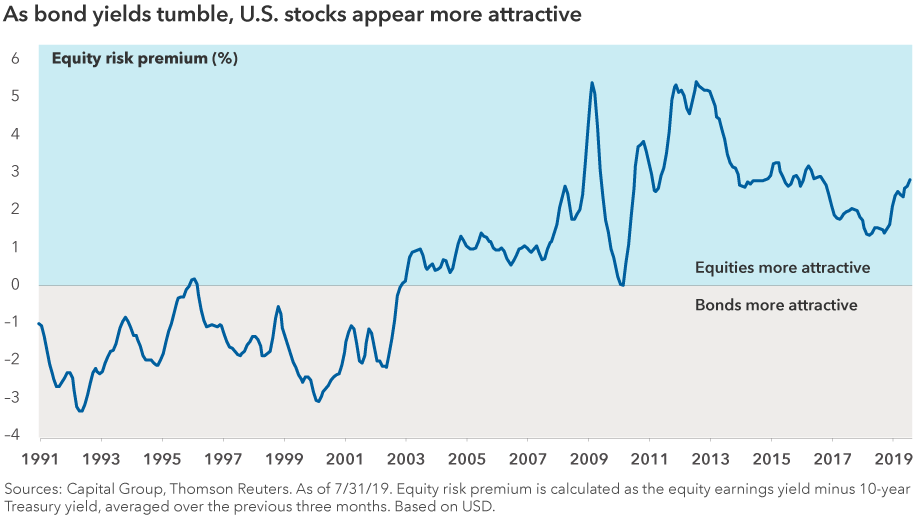

In this declining rate environment, are stocks or bonds more attractive?

Spence: For most of this year, we’ve seen stocks and bonds rally at the same time. That’s not likely to continue. Barring a recession, we think adding U.S. equity exposure makes more sense in this environment. The Fed is adding monetary fuel to a growing economy, and that could propel risky asset prices higher, while it would be difficult for bond yields to move a lot lower than what is already priced into the market. Yes, equity valuations are relatively high, but lower bond yields help support those higher valuations.

Do you think U.S. stocks will end the year in positive territory?

Franz: Fed officials seem determined not to go against market expectations, so there is a good chance they will continue to ease, providing a favorable environment for stock prices to drift higher. Although U.S. corporate earnings have turned down slightly, 76% of S&P 500 companies have, as of August 9, reported second-quarter earnings per share above consensus estimates, so that bodes well for the earnings outlook.

Overall, U.S. markets and the economy appear to be taking the trade dispute in stride, at least for now. Even with the announced tariff increases in early August and China’s currency manipulation, U.S. stocks are still up more than 17% on a year-to-date basis, and I expect double-digit gains to hold up through the end of the year.

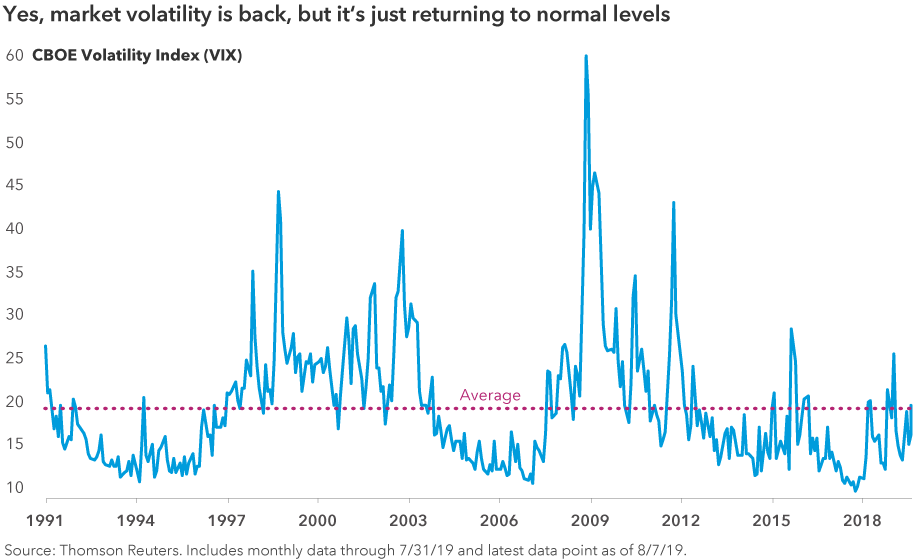

Until some sort of trade compromise is reached, market volatility will likely remain elevated, but even that metric needs to be put in perspective. At current levels, the higher volatility we’ve seen recently is simply a return to normal after a period of relative calm. Those days appear to be over for now.

Barring a full-blown trade war, do you think a U.S. recession is on the horizon during the next few years?

Spence: We’ve been saying for quite a while now that the U.S. is exhibiting classic late-cycle economic conditions. At some point, this remarkable 11-year expansion will come to an end. But if we can avoid a trade war, and if the Fed continues to stimulate the economy, then it would not be surprising to see another year or two of uninterrupted growth. We could experience a downturn in 2021, but that’s really just a placeholder for now as we continue to evaluate key economic indicators. As the Fed likes to say, the outlook remains data dependent.

Investment implications

- Where appropriate, maintain a balanced portfolio of stocks and bonds. Stocks have higher potential, but given greater uncertainty emanating from trade disputes, downside protection is important.

- Equity portfolios should be diversified between U.S. and non-U.S. as well as growth and dividend-oriented stocks. In any market pullback, growth stocks tend to suffer sharper declines.

- Ensure bond portfolios are not excessively exposed to credit, which tends to move in the same direction as stocks. Bond portfolios should have a low correlation to equities.

Learn more about

Investing outside the United States involves risks, such as currency fluctuations, periods of illiquidity and price volatility, as more fully described in the prospectus. These risks may be heightened in connection with investments in developing countries.

The return of principal for bond funds and for funds with significant underlying bond holdings is not guaranteed. Fund shares are subject to the same interest rate, inflation and credit risks associated with the underlying bond holdings. Lower rated bonds are subject to greater fluctuations in value and risk of loss of income and principal than higher rated bonds.

Our latest insights

-

-

Economic Indicators

-

Demographics & Culture

-

Emerging Markets

-

Never miss an insight

The Capital Ideas newsletter delivers weekly insights straight to your inbox.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the mutual fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only. Use of this website and materials is also subject to approval by your home office.

Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.