Chart in Focus

Categories

Market Volatility

4 ways to stay calm when markets stumble

KEY TAKEAWAYS

- Shock events such as the coronavirus outbreak and related stock market volatility can cause investors and 401(k) plan participants to act on their emotions.

- Putting a plan in place when markets turn south — and reviewing that plan when emotions are running high — can temper this impulse.

- The current market volatility gives investors, advisors and plan sponsors a golden opportunity to talk about what to do — or not do — if there is a sustained downturn.

In the eyes of veteran financial advisor Tim McCabe, there is no better time to talk about market shocks than right here, right now.

So on February 28, just as news media were reporting the spread of the coronavirus to Italy and South Korea — and the Standard & Poor’s 500 Composite Index was finishing a seven-day slide of more than 12% — McCabe and a colleague met with a young client to discuss his investments, the news of the day and the related market volatility.

This client, who had just begun investing a few years ago and had never experienced a significant market downturn, was visibly uneasy. “I addressed the troubling news head-on,” recalls McCabe, owner and principal of McCabe & Associates outside Chicago. “I emphasized that I cannot tell him how the coronavirus will impact the market or economy because I don’t think anybody knows.”

Instead, McCabe encouraged his client to focus on the long-term plan they had developed, and then he took some time to offer historical perspective. “I told him that Covid-19 may be new, but market volatility is not,” says McCabe. “And that patient investors who stay the course have tended to do better over time.”

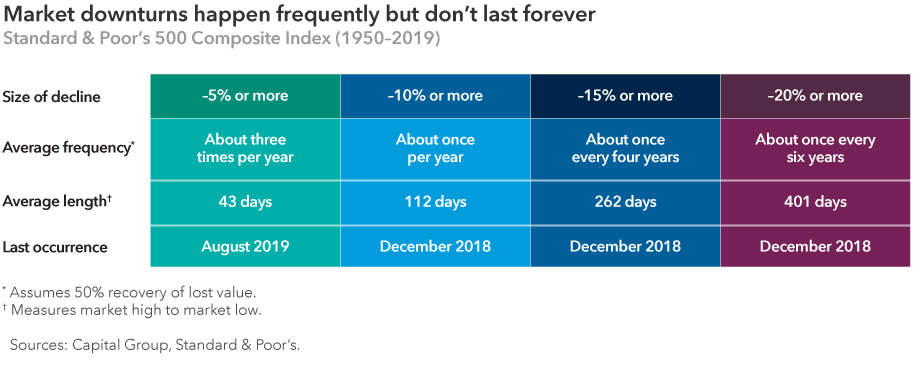

He shared data confirming that market downturns are inevitable but that markets have bounced back from crises in the past. Indeed, market corrections (a decline of 10% or more) have happened about once every year, according to S&P 500 data from 1950 to 2019.

“But facts alone won’t work,” says McCabe. “You’ve got to acknowledge their feelings too.” It didn’t hurt that this particular investor was the son of a client McCabe had been working with since the 1980s. “I was able to drive the point home by sharing some experiences I had with his father through market cycles.”

No doubt, conversations like this are taking place all over the country. Here are four key steps that you can take to counteract market volatility and act as an antidote to the breathless media coverage of the coronavirus’s spread.

1. Keep the conversation going — in good times and bad

First and foremost, don’t wait for a bear market or a full-blown economic crisis to get the conversation going. Reaching out in both good times and bad to acknowledge the inevitability of market shocks can help temper emotions.

McCabe’s firm keeps the conversation going by regularly posting articles to the firm’s website. “We use it to provide updates about market developments,” McCabe says. “We have enhanced it over the years, and it has been a useful tool to keep in regular contact with investors.”

Similarly, McCabe’s firm— which also works with qualified retirement plans — provides plan sponsors with timely articles and information they can distribute to employees. “We try to keep these communications simple and straightforward, because many plan participants typically don’t spend much time reviewing their 401(k) investments,” he says. “We use times like these to remind plan participants of the potential benefits of using target date funds, which relieves the participant of the burden of rebalancing their portfolios, something that is critical after a year like 2019 when stocks far outpaced bonds.”

As often as possible, advisors should reinforce the notion that the journey will inevitably be bumpy. When equities first began their February swoon, Brian Jones, chairman at CJM Wealth Advisers in Fairfax, Virginia, like many other advisors, sent emails to clients to acknowledge the market losses and offer a bit of perspective on the plunging red arrows they saw flashing on television.

“It is important not to give in to the temptation to make sudden moves during market downturns,” CJM said in a recent note to clients. “Your broadly diversified portfolios are designed to participate in the gains when the market is rising and to minimize, as much as possible, the declines when markets sell off.”

2. Revisit your long-term plan

Having a long-term investment plan conceived during more benign times and revisiting that plan when markets tumble can help investors keep their emotions in check. “Every year we schedule reallocation discussions with clients,” notes McCabe. “When we do, we ask if their goals have changed. If not, we strongly advise them to stick with the long-term plan we developed together.”

Planning for a rainy day helps investors stay calm says Suresh Raghavan, a registered investment advisor (RIA) and principal at MBR Financial in Houston. Raghavan works with clients to create an estimate of monthly living expenses and then puts enough away in cash or cash equivalents to cover 18 months’ worth of those bills.

Even if the client doesn’t have to dip into these funds, just knowing they’re there can help calm frazzled nerves. “My partners wish I wouldn’t call it this, but I call it the ‘blankie’ portfolio: It’s to help you sleep well at night,” Raghavan says.

3. Place current events in historical perspective

Keeping a long-term perspective is always important, but it’s essential when markets are stormy and emotions running high. A look at history shows that while markets react to news events in the short term, they have tended to reward patient investors over long periods of time.

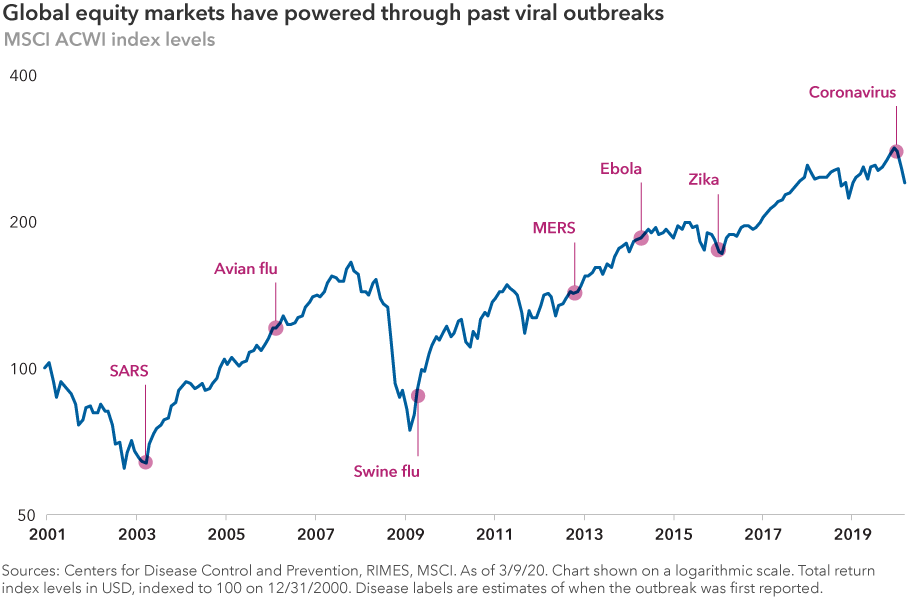

Indeed, global markets have shrugged off the impact of past viral outbreaks. While the past is not predictive of the future, it does offer valuable perspective.

“History may not repeat, but it does rhyme,” notes McCabe. “There is nothing exactly like the coronavirus. We don’t really know how this is going to play out. But you can compare it to SARS to help put things in perspective. What have we seen in the past that may help us look at current conditions more rationally?”

No one knows how long or how far the coronavirus will spread, but here is a brief look at how three recent infectious outbreaks unfolded:

- 2003 — SARS saw 8,000 people infected. It was brought to an end by good hygiene (hand-washing) and environmental factors (warming temperatures), and it burnt out when enough people became infected to build an immunity to the disease.

- 2009 — H1N1 Flu caused a pandemic in ‘09 and has become a seasonal flu, usually recurring in the colder months.

- 2014 — Ebola in West Africa ended with human intervention, when the WHO declared a coordinated international response. Countries worked together to administer to the sick, and when a second outbreak occurred in 2018, human intervention made the difference again when treatments developed from the first outbreak were offered to patients.

4. Acknowledge the power of emotions

At the end of the day, we are all emotional beings. A key finding of behavioral economists is that people often act irrationally when making investment choices. “Individuals deal with money very viscerally,” notes Raghavan. So naturally they will expect their advisors to respond with more than just historical market data.

The key is to put current activity into the context of the bigger picture and to acknowledge that biases can affect investor thinking. These factors may lead investors to believe that markets are doing worse or better than impartial analysis would reveal:

- Confirmation bias: Giving more weight to trends you already believe in

- Availability bias: Giving more weight to recent events

- Framing effect: Letting the presentation of information affect your interpretation of it

A good advisor should acknowledge investors’ fears, Raghavan says, but remind them that there are “always going to be things we don’t know, things we can’t predict.”

Like McCabe, Raghavan says he’s generally been able to rely on his three decades of experience to help reassure jittery investors. “When you’re flying in a plane and there’s turbulence, what should you do?” Raghavan asks.

The last thing passengers should do is to try to fly the plane themselves, he adds. “Clearly, you want to make sure the plan is appropriate for the situation,” he says. “But allow the professional to do what the professional does,” and guide that investor through the storm.

Learn more about

Investing outside the United States involves risks, such as currency fluctuations, periods of illiquidity and price volatility, as more fully described in the prospectus. These risks may be heightened in connection with investments in developing countries. Small-company stocks entail additional risks, and they can fluctuate in price more than larger company stocks.

Standard & Poor’s 500 Composite Index is a market capitalization-weighted index based on the results of approximately 500 widely held common stocks. Standard & Poor’s 500 Composite Index (“Index”) is a product of S&P Dow Jones Indices LLC and/or its affiliates and has been licensed for use by Capital Group. Copyright © 2020 S&P Dow Jones Indices LLC, a division of S&P Global, and/or its affiliates. All rights reserved. Redistribution or reproduction in whole or in part is prohibited without written permission of S&P Dow Jones Indices LLC.

The MSCI ACWI is a free float-adjusted market capitalization-weighted index that is designed to measure equity market results in the global developed and emerging markets, consisting of more than 40 developed and emerging market country indexes. MSCI has not approved, reviewed or produced this report, makes no express or implied warranties or representations and is not liable whatsoever for any data in the report. You may not redistribute the MSCI data or use it as a basis for other indices or investment products.

The market indexes are unmanaged and, therefore, have no expenses. Investors cannot invest directly in an index.

Our latest insights

-

-

Economic Indicators

-

Demographics & Culture

-

Emerging Markets

-

related insights

-

Markets & Economy

-

U.S. Equities

-

Technology & Innovation

Never miss an insight

The Capital Ideas newsletter delivers weekly insights straight to your inbox.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the mutual fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only. Use of this website and materials is also subject to approval by your home office.

Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.