Chart in Focus

Categories

Monetary Policy

Help wanted: How a distorted job market may foil the Fed

Jared Franz

Jared Franz

November 16, 2021

Much has been said and written about rising inflation and how it might influence the Federal Reserve’s monetary policy. A 30-year high in the U.S. consumer price index in October is only fueling expectations that the Fed will raise interest rates in earnest beginning next year.

But what about the labor market? Given the central bank’s dual mandate to promote “maximum employment” along with “stable prices and moderate long-term interest rates,” it would be hard to gauge the pace of monetary policy tightening without a clear picture of the many disruptions affecting U.S. workers and employers.

It’s striking how much has changed in the U.S. labor market. Prior to the pandemic, the unemployment rate sat at a 50-year low of 3.5% and wage growth was stable. Now the market is rife with mismatches between labor supply and demand. The unemployment rate has declined considerably from double-digit levels in the early months of the pandemic, but job openings have soared to a record high, above 10 million. The so-called Great Resignation has seen millions of people leave their jobs, and the labor force participation rate sits at 1970s levels. Also, wages are marching higher. This is not the labor market the Fed expected to see 18 months after the COVID-19 recession ended in April 2020.

The key question is whether these are temporary dislocations that will subside as the pandemic wanes, or evidence of a lasting shift in the U.S. labor market.

In my view, COVID-19's impact on labor markets is more structural than cyclical. Many companies that have survived the pandemic on reduced staff are likely leaner, meaner and more efficient. They are unlikely to need the same employment levels they had in February 2020. Likewise, from a labor point of view, many workers do not want the jobs they had before the pandemic. They are taking this opportunity to reassess careers, work-life balance and the need for flexibility. These changes, both cyclical and structural, will weigh on Fed policymakers’ decisions in the months ahead and present a difficult policy choice: raise interest rates to reduce inflation or keep rates low to support full employment.

Temporary mismatches could be resolved soon

To be sure, there are cyclical aspects to the labor market. So, as the pandemic wanes, I expect employment to return to more typical levels in the sectors that were hardest hit by pandemic-related disruptions. Similarly, people who are out of work due to a lack of dependable child care, or who are pursuing education or retraining, could return relatively soon.

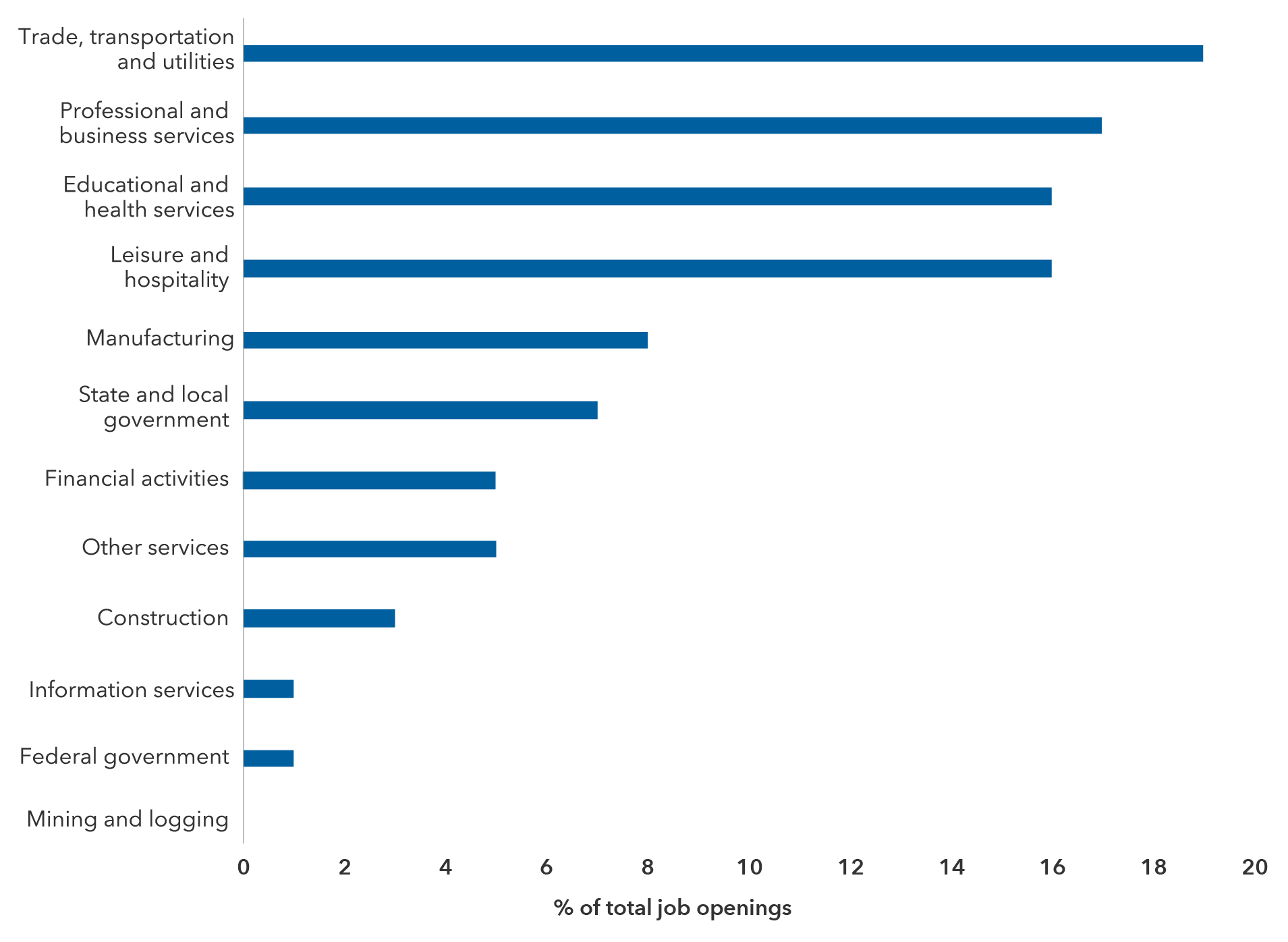

Most job openings are in four COVID-19–impacted sectors

Sources: Capital Group, Haver. Data as of August 2021. Figures may not add up to 100% due to rounding.

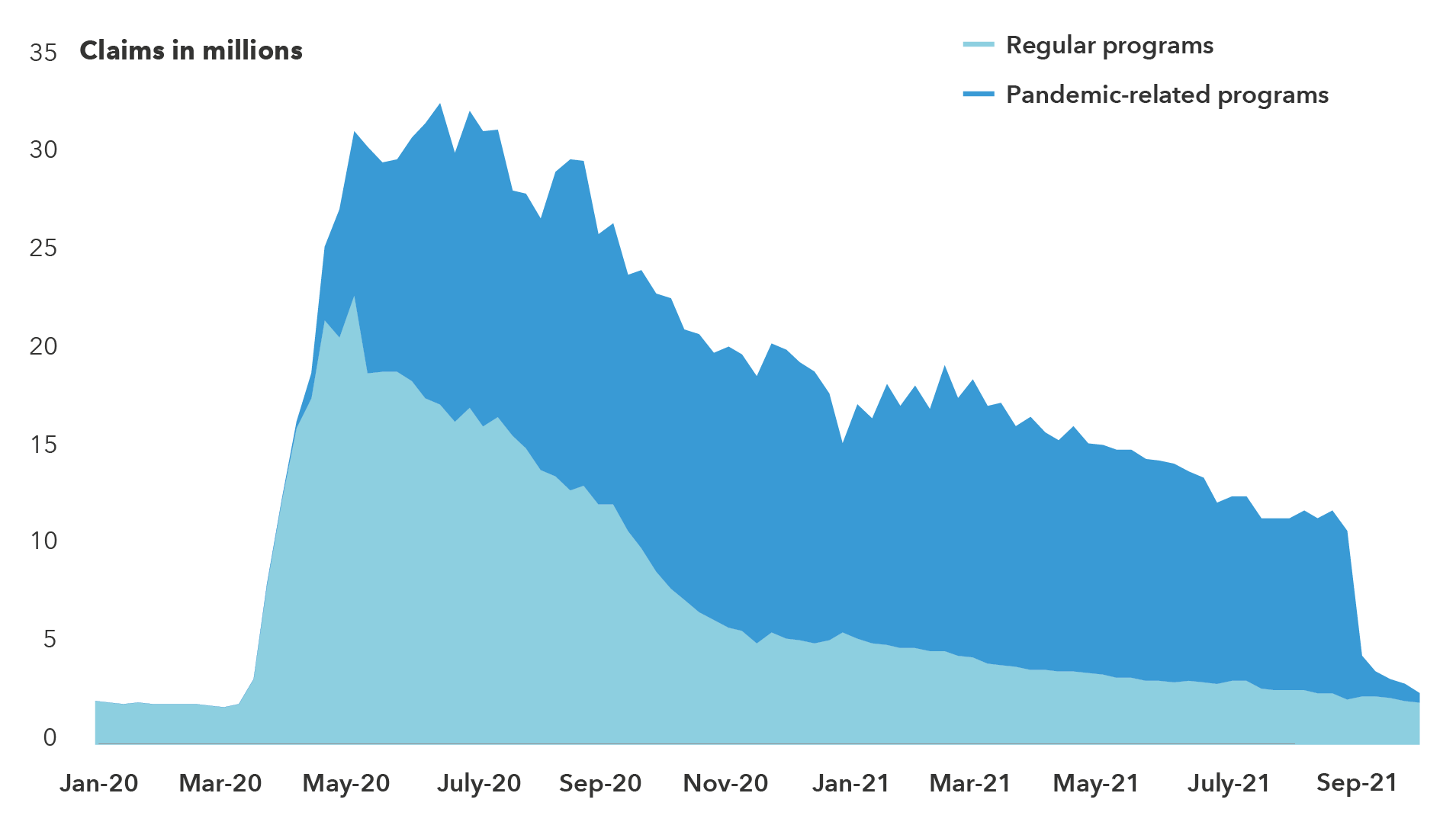

As employers in these sectors find it easier to fill jobs, we’re likely to see a slowdown in wage gains and the one-time bonuses they have been offering to attract workers. We may even see a temporary rise in the unemployment rate, which would be a good sign if it meant that more people were coming off the sidelines and actively seeking jobs. It may turn out that the sharp drop in continuing unemployment insurance claims, which followed the expiration of federal emergency unemployment benefits in early September, will mark a turning point in the labor market recovery.

Unemployment insurance claims plunged in September after peaking near 33 million

Sources: Capital Group, U.S. Department of Labor, Haver. Data as of October 9, 2021.

Structural disruption extends beyond the COVID-19–impacted sectors

However, even as some parts of the labor market normalize, a large group of workers is unlikely to respond to these cyclical improvements. The path to normalization is likely to be bumpy as millions of businesses and households reassess their demand for workers and desire for jobs, respectively. I’ve reached this conclusion after our research revealed a surprising amount of labor market disruption across multiple economic sectors, a pattern that extends well beyond pandemic-centric sectors and into areas that are more insulated from COVID-19.

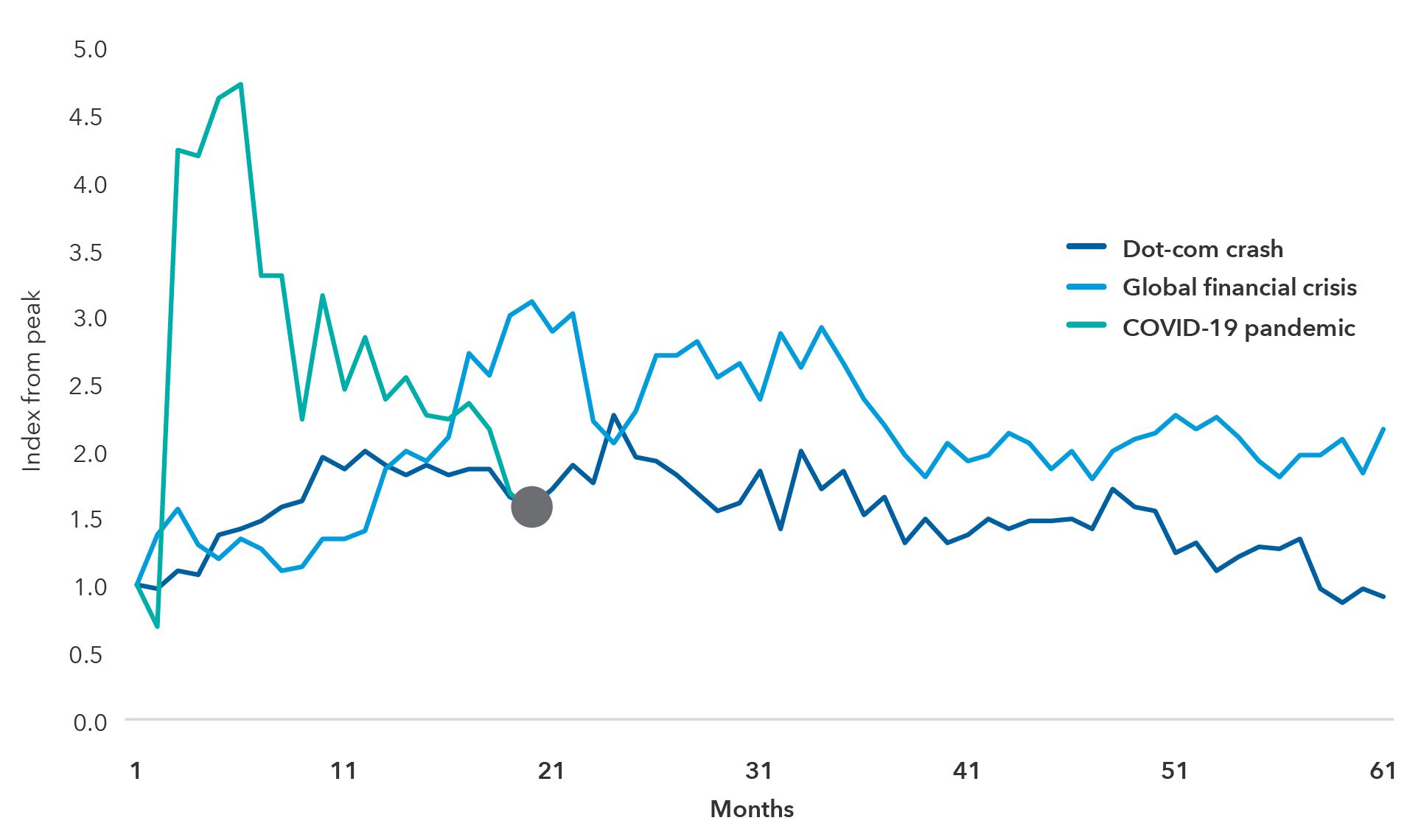

A good example is the information sector, which includes publishing, broadcasting and telecommunications, among others. It has probably been least impacted — and arguably has been supported — by the pandemic because so many people have been working from home. Yet changes in the sector’s unemployment rate are consistent with the 2001 recession that followed the bursting of the dot-com bubble. And, although job openings are elevated, it is surprising that we have not seen stronger wage gains. Another sector with similar dynamics is construction, where wage gains have been strong in absolute terms. However, when measured against prior recoveries, they are less striking. The reasons for this are still unclear, and this is an area that needs more research.

Change in the information sector’s unemployment rate near dot-com crash level

Source: U.S. Bureau of Labor Statistics. COVID-19 pandemic data as of September 2021.

Note: Chart displays changes in the unemployment rate for the information sector during three periods. All three periods shown are indexed to 1, which represents the unemployment rate in the month prior to the start of the respective recessions as determined by the National Bureau of Economic Research. The recessions began in November 2001 (dot-com crash), June 2009 (global financial crisis) and February 2020 (COVID-19 pandemic).

More broadly, it’s worth noting that the recovery in the labor force participation rate, which includes people actively entering the workforce, has been much slower than the recovery of the unemployment rate, which can move up and down a lot depending on near-term factors. This appears to support the idea that structural forces are making a full normalization of the labor market more challenging.

Fed Chair Jerome Powell acknowledged this challenge in his remarks following the Fed’s November meeting: “We thought that schools reopening and elapsing unemployment benefits would produce some sort of additional labor supply. That doesn't seem to have been the case, interestingly.” He said it was a trend the central bank would watch closely.

Capital Ideas™ webinars

Insights for long-term success

CE credit available

Structural factors could keep many out of work past 2022

What we've seen historically is that the labor market often bears the brunt of big disruptions, such as the global financial crisis. Just as some construction workers may have become baristas during the U.S. housing crisis, now it may be baristas transitioning into construction work as the hospitality sectors remain soft. These shifts take time, however, which makes me skeptical of the Fed’s base case of getting back to full employment in 2022.

Furthermore, some of the millions of job openings could be automated away rather than filled by returning workers. Think QR code menus replacing restaurant servers or machines making french fries. This is already happening to some extent, as companies adapt to the new normal and learn to function without hiring extra staff.

But automation isn’t the only thing that could keep the unemployed out of work longer. Consider those whose prospects have dimmed because they are now competing against a global workforce that is even more tightly interconnected by technology, or who now have a skill or geographic mismatch with available jobs. At the extreme are those who have reassessed their careers or accelerated retirement and are less likely to ever return to the workforce. Although many of those affected by cyclical factors are likely to return to work by early next year — barring a resurgence of COVID-19 cases — people whose reasons are more structural may not return until 2023, if at all.

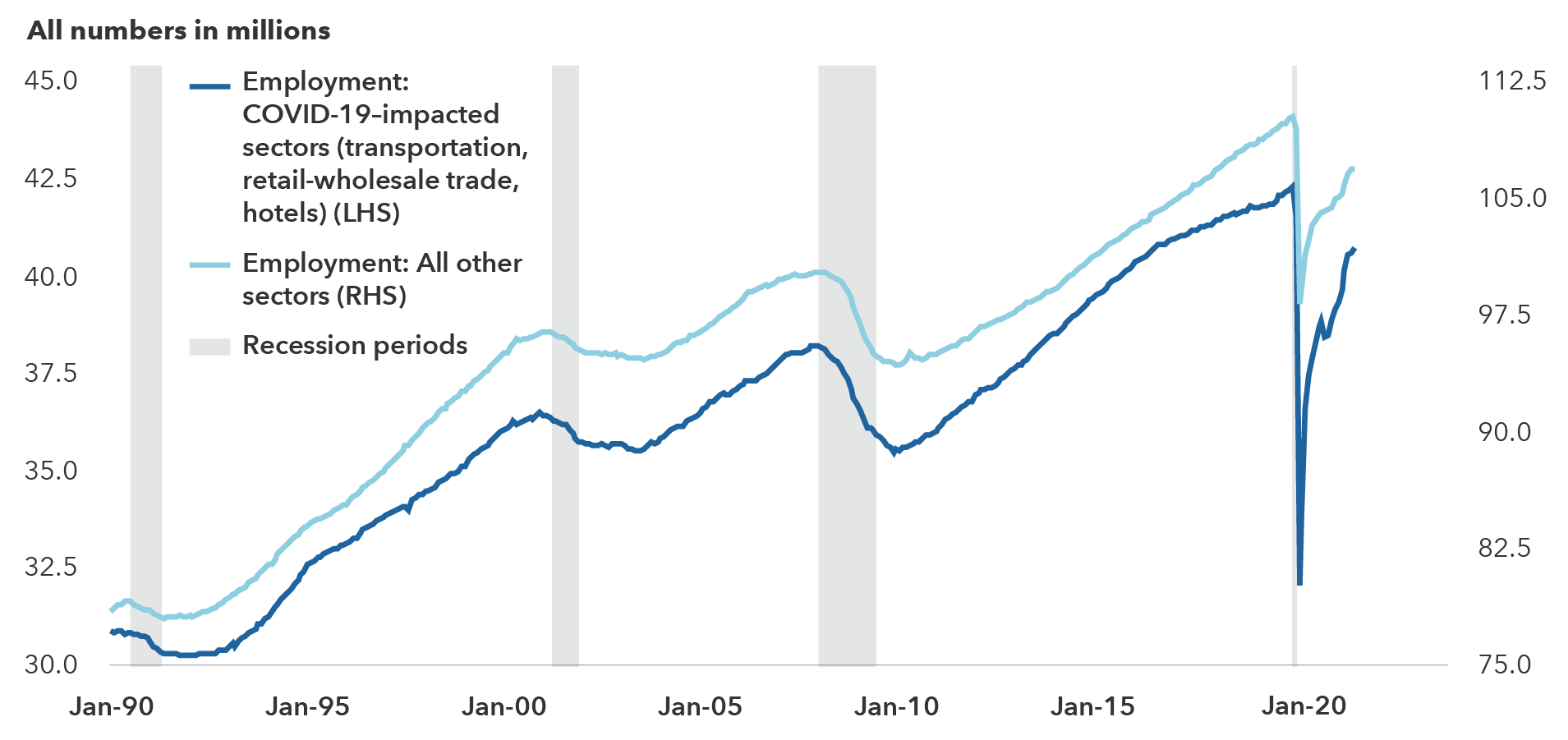

Employment grinding toward a full recovery

Sources: Capital Group, Haver. Data as of September 2021. Shaded areas represent recession periods as determined by the National Bureau of Economic Research.

Implications for the Fed

Today, the Federal Reserve faces a knotty challenge: Surging inflation is driving pressure for higher interest rates, which could stymie growth and weaken the labor market recovery. Unless the economy is able to absorb the large supply of labor that is currently sidelined and the labor force participation rate recovers to pre-pandemic levels, it seems unlikely that the U.S. unemployment rate will regain its pre-pandemic low of 3.5% by 2023. I think it will take until 2024.

At its November 3 meeting, the Fed confirmed that it will begin scaling back its $120 billion-per-month asset purchase program, starting in late November. Meanwhile, the Treasury market is pricing in rate hikes by mid-2022. While the persistence of high inflation in recent data could push the Fed down that path, the challenges in labor markets could temper its pace.

Compounding the Fed’s dilemma is that a large part of the inflationary pressure is coming from supply constraints rather than demand. This pandemic shock is turning the “divine coincidence” — the idea that most negative shocks to the economy come from the demand side — on its head. In a traditional scenario, as the economy is gaining steam, the central bank can combat rising prices by lifting interest rates, which cools the economy and the labor market, in turn dampening demand. But in the current situation, lifting rates would dampen inflation but also further set back the labor market. This could create the risk of more structural dislocation in the labor market, confounding the Fed’s dual mandate of price stability and full employment.

That said, if the factors weighing on the labor market turn out to be more cyclical, the unemployment rate could be back to 3.5% more quickly than I expect and interest rates would need to be higher. In that case, the Fed may need to accelerate tightening. If it’s more structural, then the unemployment rate could remain elevated and be slow to fall. Here the Fed would be slower to raise rates.

Learn more about

Our latest insights

-

-

Economic Indicators

-

Demographics & Culture

-

Emerging Markets

-

RELATED INSIGHTS

-

Economic Indicators

-

-

Chart in Focus

Never miss an insight

The Capital Ideas newsletter delivers weekly insights straight to your inbox.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the mutual fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only. Use of this website and materials is also subject to approval by your home office.

Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.