Chart in Focus

Categories

Market Volatility

Greater volatility likely as fiscal stimulus pairs with monetary tightening

KEY TAKEAWAYS

- The net impact of reduced monetary accommodation and rising fiscal stimulus is leading to a period of higher volatility.

- Inflation has been modest in recent years but may increase as resource utilization rises.

- Tight credit spreads imply asymmetric downside risk, even amid economic expansion.

We continue to be in a Goldilocks period for the global economy. Growth across most regions is running modestly above trend, while inflation is gradually moving higher but remains tame. However, this equilibrium is at the risk of being disrupted as central banks around the world begin to tighten monetary policy while U.S. lawmakers move forward with a strong dose of fiscal stimulus via tax cuts.

Capital Group’s Portfolio Strategy Group Forum (PSG) takes place three times each year. The two-day event brings together the entire fixed income group from across the globe for an in-depth discussion on the macroeconomic environment and fixed income markets. Our proprietary fundamental research is the foundation of the discussions and any recommendations for our investment professionals that result from these meetings. This is a recap of views that emerged from the recent meeting in late February.

Outlook and positioning

The economic backdrop looks positive. U.S. growth is expected to be above 2.5% in 2018 with momentum likely through 2019. In Europe, economic expansion is broadening beyond the core economies and should remain around 2% over the next two years. Meanwhile, China should be able to sustain a growth rate above 6% in 2018 but will likely slow next year as the government implements more aggressive economic and credit reforms.

Thus far, the uptick in global growth has left core inflation below central bank targets. However, years of modest but steady growth have begun to push resource utilization rates higher, which should put upward pressure on prices. Recent weakening of the U.S. dollar and rising shelter costs, a major component of the Consumer Price Index, are also lifting inflation.

Tax reform and the proposed budget, known as the Tax Cuts and Jobs Act and the Bipartisan Budget Act respectively, are likely to push the U.S. economy further away from equilibrium and increase fiscal deficits. Lower corporate tax rates should boost capital expenditures and put some upward pressure on resource utilization. Yet it is not clear that this will lead to higher productivity.

Central bank policy has already begun shifting in the U.S. and will begin shifting in Europe in 2018. Quantitative easing, or QE, in the U.S. is shifting to quantitative tightening. Asset purchases by the European Central Bank are expected to slow in the third quarter. As monetary policy tightens, we are seeing a rise in market volatility.

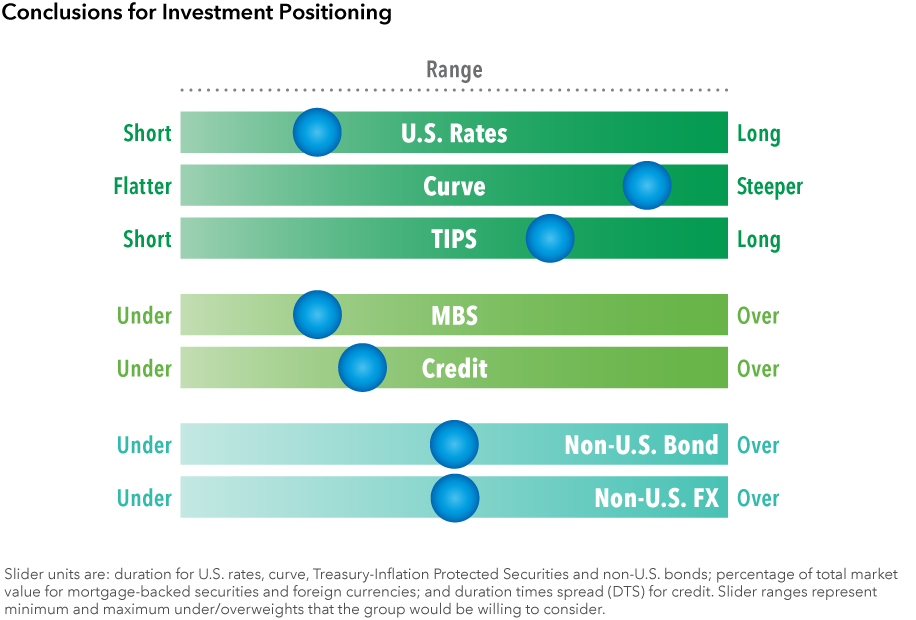

Our portfolio positioning recommendation to managers seeks to outpace the Bloomberg Barclays U.S. Aggregate Index in a more uncertain world of higher market volatility. It aims to accomplish this while giving up very little yield relative to the index. Core interest rate positioning – both duration and curve positioning – seeks to balance potential market outcomes and the path of rates that is already priced into forward markets.

Credit

Although the economic backdrop remains constructive, the extended period of low interest rates has encouraged corporations to increase leverage and investors to reach for yield. The risk for both investment-grade and high-yield credit is asymmetric at this point in the cycle with limited room for spread tightening and high potential for more volatility and spread widening. While default rates in high yield are not expected to rise significantly in the next year, companies will need to begin addressing their debt structures ahead of the next recession. As a result, we favor an underweight position in credit.

Duration

Duration positioning is driven by a number of factors, including the current shape of the spot and forward yield curves, our outlook for economic conditions and anticipated central bank policy. While economic growth is improving and central banks are beginning to react, they may not move quickly enough in an environment of persistent cyclical strength. In this scenario, yields are likely to move higher than is anticipated by the forward curve. Thus, core bond portfolios should be modestly short duration, but positioned for a steepening yield curve.

Yield curve

In the last 12 months, there has been a significant flattening of the U.S. yield curve as investors have anticipated continued tightening by the Federal Reserve. As a result, the five-year part of the U.S. yield curve is relatively attractive. While further yield curve flattening could occur, much of this is discounted in the forward markets already. Increasing issuance of U.S. Treasury bonds combined with Fed tightening could also put pressure on longer dated maturities. Thus, managers should position portfolios for yield curve steepening by being long the five-year part of the curve and underweight 10-year and 30-year bonds.

Inflation

Although breakeven inflation rates have moved higher, the risks are still to the upside in the U.S. as resource utilization increases with core inflation potentially reaching 2.5%. Treasury Inflation-Protected Securities (TIPS) are also likely to offset the core bond credit position in an environment where credit continues to rally. Core bond portfolios should be overweight U.S. TIPS.

Mortgages

Mortgage spreads remain tight with primary rate volatility still low. Spreads have little room to tighten further. The Fed will begin to increase the pace of its quantitative tightening in the second quarter of 2018, which will put upward pressure on supply. Therefore, core bond portfolios should have a less-than-index position in mortgages.

Learn more about

Our latest insights

-

-

Economic Indicators

-

Demographics & Culture

-

Emerging Markets

-

Related Insights

Never miss an insight

The Capital Ideas newsletter delivers weekly insights straight to your inbox.

Investments are not FDIC-insured, nor are they deposits of or guaranteed by a bank or any other entity, so they may lose value.

Investors should carefully consider investment objectives, risks, charges and expenses.

This and other important information is contained in the mutual fund prospectuses and summary prospectuses, which can be obtained from a financial professional and should be read carefully before investing.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.

All Capital Group trademarks mentioned are owned by The Capital Group Companies, Inc., an affiliated company or fund. All other company and product names mentioned are the property of their respective companies.

Use of this website is intended for U.S. residents only. Use of this website and materials is also subject to approval by your home office.

Capital Client Group, Inc.

This content, developed by Capital Group, home of American Funds, should not be used as a primary basis for investment decisions and is not intended to serve as impartial investment or fiduciary advice.

Statements attributed to an individual represent the opinions of that individual as of the date published and do not necessarily reflect the opinions of Capital Group or its affiliates. This information is intended to highlight issues and should not be considered advice, an endorsement or a recommendation.