Fundamentals of private credit

This video dives further into private credit, its opportunities and its risks. In particular, you'll learn about direct lending and asset-based finance, two major categories of private credit.

This video dives further into private credit, its opportunities and its risks. In particular, you'll learn about direct lending and asset-based finance, two major categories of private credit.

Global credit & markets investment strategist at KKR

9MINVIDEO

Select each resource below to learn more.

Direct Lending and ABF

What is senior direct lending?

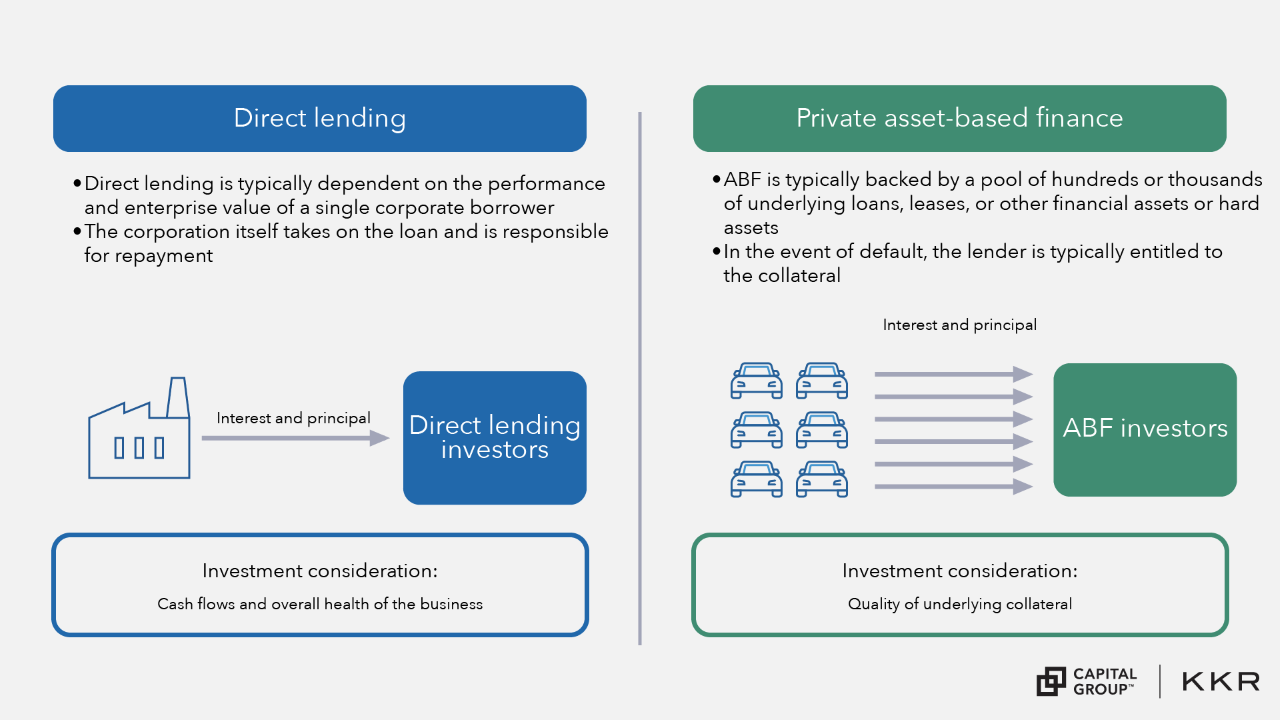

Senior direct lending is a specialized form of private credit in which lenders provide senior loans directly to upper-middle and middle-market companies under mutually agreed terms, and are based on the business's cash flows, value, and overall health. These loans can be made for various business needs, including buyouts, refinancing, recapitalization or to fund growth initiatives.

Senior direct loans sit on top of a borrower’s capital structure and are the first to be prioritized in the event of default, thus seeking to lower the potential for loss. Unsecured loan holders are repaid next. (You can learn more about a company’s capital structure in this lesson’s next reading.)

Direct lending’s potential benefits (to the different parties)

Direct lending is a private credit lending transaction that typically involves three parties: investors, a private credit investment fund and borrowers. Senior direct loans are mostly held-to-maturity, so value is created by a manager's ability to originate, underwrite and structure loan deals. The debt instruments purchased by the fund are subject to the risk that a borrower will default on the payment of principal, interest or other amounts owed. The benefits of direct lending to borrowers and investors include:

For borrowers:

For investors:

What is asset-based finance?

Asset-based finance is a broad form of non-corporate lending backed by a variety of collateral, including tangible and financial assets. This collateral often generates cash flows and can act as a form of protection for the lender in the event a borrower does not meet its payment obligations.

Four major categories of collateral within asset-based finance, include:

The potential benefits of ABF

Backed by large pools of collateral, ABF may benefit investors with predictable cash flows and low correlations to a range of public and private assets. There are risks associated with ABF — including fluctuating collateral values that can shift with market conditions. ABF investments differentiate from traditional public market investments in that they are privately originated and negotiated and may benefit from the potential to be structured in many ways.

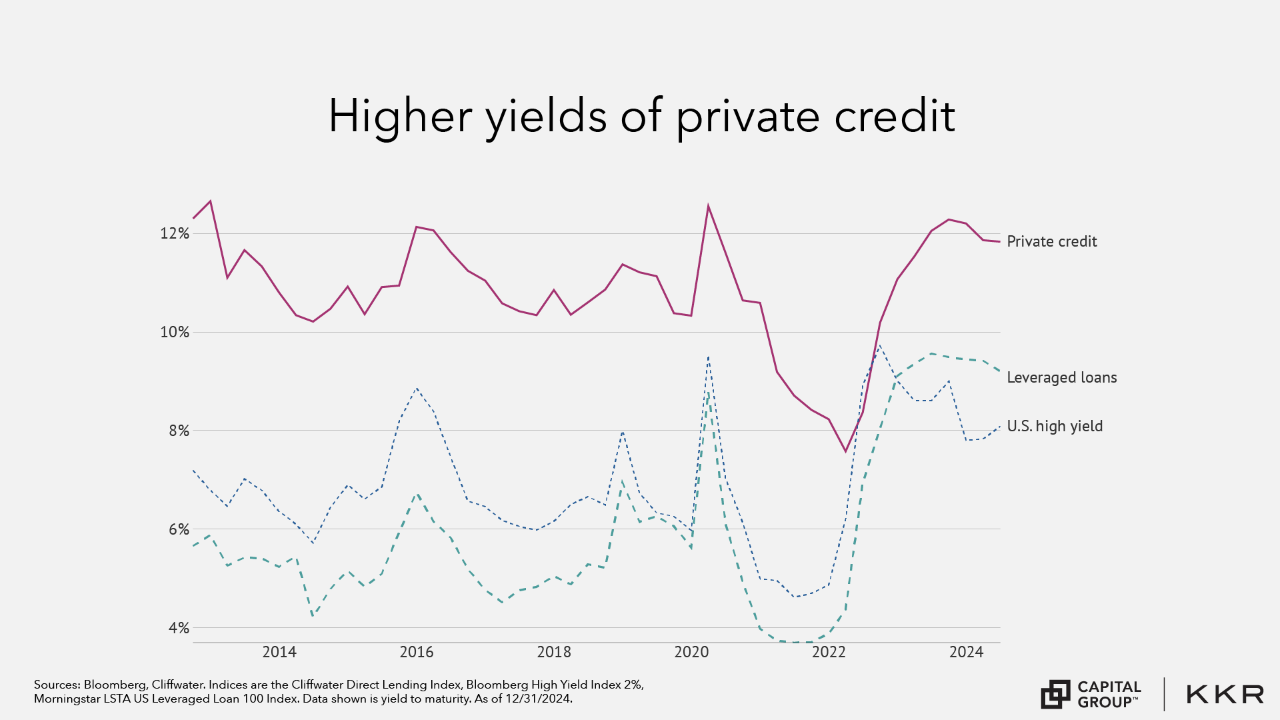

Private credit can offer potentially higher income than traditional fixed income investments, compensating for the increased credit and illiquidity risk. The largest part of the private credit universe is senior direct lending, and it is generally considered to be less risky than other types of private credit investments.

Senior direct lending is a specialized form of private credit in which lenders provide loans directly to middle-market companies under mutually agreed terms and are typically backed by the financial health and cash flows of the borrowing company. These loans can serve business needs like buyouts, refinancing, recapitalization or growth initiatives.

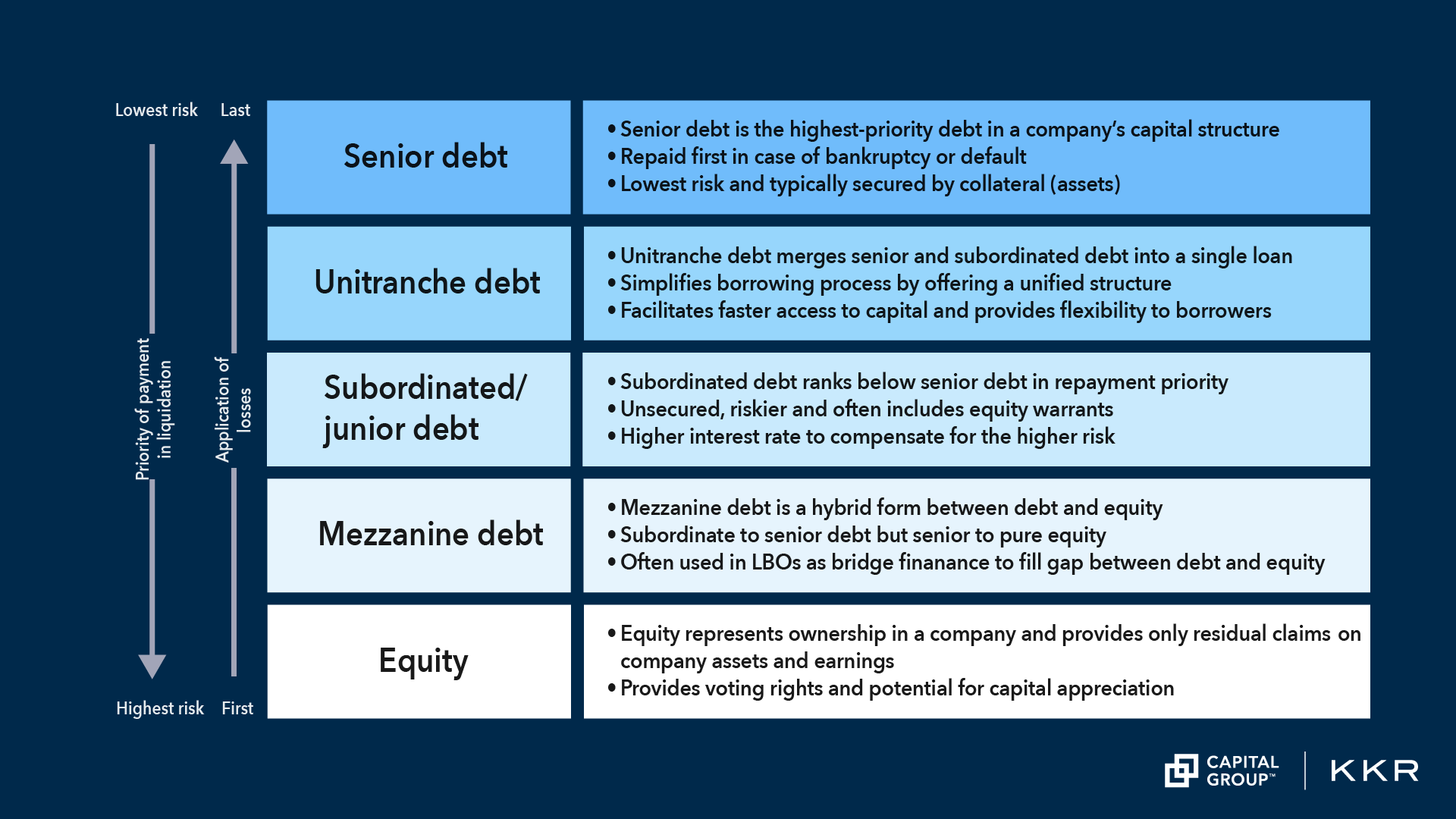

Understanding the “capital structure”

What makes a loan “senior?” Senior loans sit atop a company’s capital structure — the hierarchy of claims on a company’s assets that is defined by the sources of a company’s financing, i.e., debt and equity. Not every borrower’s capital structure includes all the layers in the illustration, but senior debt sits at the top by definition.

The higher a source of financing sits in the capital structure, the higher its priority on claims in the event of default or liquidation — and the less risky it is generally to invest in.

For example, in the illustration, equity sits at the bottom of the capital structure. It’s the most financially risky of these layers but also has the highest return potential because it represents an ownership stake in the company. If the company were to liquidate its assets in bankruptcy, the equity shareholders would be the most likely to suffer the greatest loss.

Above equity sit various levels of credit. Subordinated debt ranks above equity but below senior debt. If a company goes bankrupt, subordinated debt holders are paid by remaining funds after senior debt holders and before equity holders.

With senior credit at the top of the capital structure, this means that in the event of liquidation, the senior creditors would be the highest repayment priority, making holding senior credit the least risky layer of the capital structure. Senior debt is also typically secured by collateral, which means if the borrower cannot meet its obligations, the lender has the legal right to recover the outstanding debt by liquidating the collateral.

“Least risky,” of course, does not indicate that there is no risk at all. Even senior creditors may suffer losses in a serious bankruptcy. However, if you’re investing in the private credit market, senior direct lending is normally among the less risky segment.

You should now have a greater understanding of private credit. Don’t forget to review lesson takeaways here.

In the next lesson, you'll learn about interval funds, a vehicle that can open up access to private credit investment.

The Cliffwater Direct Lending Index was launched on September 30, 2015. Data before this date is hypothetical (back-tested) and based on the methodology established at that time. Adjustments during back-testing aimed to capture a comprehensive universe of securities and simulate the target market or strategy, especially during market anomalies. Back-tested performance provides historical insights but has limitations, including survivorship and look-ahead biases. Actual returns may differ significantly from back-tested results, and past performance does not guarantee future results. Index returns shown do not reflect actual trading activities and exclude sales charges or fees associated with purchasing securities or investment funds tracking the Index. Additional fees and charges may impact performance of securities or funds compared to the Index. Market risks, including financial market fluctuations, liquidity risks, and regulatory risks, may affect the Index's performance. The Index may also be subject to concentration risks if heavily weighted towards specific sectors, industries, or geographic regions.

Consider the following risks for the Capital Group KKR fund(s) discussed in this material: The fund is an interval fund that provides liquidity to shareholders through quarterly repurchase offers for up to 10% of its outstanding shares under normal circumstances. To the extent more than 10% of outstanding shares are tendered for repurchase, the redemption proceeds are generally distributed proportionately to redeeming investors (“proration”). Due to this repurchase limit, shareholders may be unable to liquidate all or a portion of their investment during a particular repurchase offer window. In addition, anticipating proration, some shareholders may request more shares to be repurchased than they actually wish, increasing the likelihood of proration. Shares are not listed on any stock exchange, and we do not expect a secondary market in the shares to develop. Due to these restrictions, investors should consider their investment in the fund to be subject to illiquidity risk.

Investment strategies are not guaranteed to meet their objectives and are subject to loss. Investing in the fund is not suitable for all investors. Investors should consult their investment professional before making an investment decision and evaluate their ability to invest for the long term. Because of the nature of the fund's investments, the results of the fund's operations may be volatile. Accordingly, investors should understand that past performance is not indicative of future results.

Bond investments may be worth more or less than the original cost when redeemed. High‐yield, lower‐rated, securities involve greater risk than higher‐rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. The fund may invest in structured products, which generally entail risks associated with derivative instruments and bear risks of the underlying investments, index or reference obligation. These securities include asset-based finance securities, mortgage-related assets and other asset-backed instruments, which may be sensitive to changes in interest rates, subject to early repayment risk, and their value may fluctuate in response to the market's perception of issuer creditworthiness; while generally supported by some form of government or private guarantee, there is no assurance that private guarantors will meet their obligations. While not directly correlated to changes in interest rates, the values of inflation-linked bonds generally fluctuate in response to changes in real interest rates and may experience greater losses than other debt securities with similar durations. The use of derivatives involves a variety of risks, which may be different from, or greater than, the risks associated with investing in traditional securities, such as stocks and bonds. For example, the fund may purchase and write call and put options on futures, giving the holder the right to assume a long (call) or short (put) position in a futures contract at a specified price. There is no assurance of a liquid market for any futures or futures options contract at any time. Investing outside the United States involves risks, such as currency fluctuations, periods of illiquidity and price volatility. These risks may be heightened in connection with investments in developing countries.

The fund invests in private, illiquid credit securities, consisting primarily of loans and asset-backed finance securities. The fund may invest in or originate senior loans, which hold the most senior position in a business's capital structure. Some senior loans lack an active trading market and are subject to resale restrictions, leading to potential illiquidity. The fund may need to sell other investments or borrow to meet obligations. The fund may also invest in mezzanine debt, which is generally unsecured and subordinated, carrying higher credit and liquidity risk than investment-grade corporate obligations. Default rates for mezzanine debt have historically been higher than for investment-grade securities. Bank loans are often less liquid than other types of debt instruments and general market and financial conditions may affect the prepayment of bank loans, as such the prepayments cannot be predicted with accuracy.

Illiquid assets are more difficult to sell and may become impossible to sell in volatile market conditions. Reduced liquidity may have an adverse impact on the market price of such holdings, and the fund may be unable to sell such holdings when necessary to meet its liquidity needs or to try to limit losses, or may be forced to sell at a loss. Illiquid assets are also generally difficult to value because they rarely have readily available market conditions. Such securities require fair value pricing, which is based on subjective judgments and may differ materially from the value that would be realized if the security were to be sold.

The fund is a non-diversified fund that has the ability to invest a larger percentage of assets in the securities of a smaller number of issuers than a diversified fund. As a result, poor results by a single issuer could adversely affect fund results more than if the fund were invested in a larger number of issuers. The fund intends to declare daily dividends from net investment income and distribute the accrued dividends, which may fluctuate, to investors each month. Generally, dividends begin accruing on the day payment for shares is received by the fund. In the event the fund's distribution of net investment income exceeds its income and capital gains paid by the fund's underlying investments for tax purposes, a portion of such distribution may be classified as return of capital. The fund's current intention not to use borrowings other than for temporary and/or extraordinary purposes may result in a lower yield than it could otherwise achieve by using such strategies and may make it more difficult for the fund to achieve its investment objective, than if the fund used leverage on an ongoing basis. There can be no assurance that a change in market conditions or other factors will not result in a change in the fund distribution rate at a future time.

“Cliffwater,” “Cliffwater Direct Lending Index,” and “CDLI” are trademarks of Cliffwater LLC. The Cliffwater Direct Lending Indexes (the “Indexes”) and all information on the performance or characteristics thereof (“Index Data”) are owned exclusively by Cliffwater LLC, and are referenced herein under license. Neither Cliffwater nor any of its affiliates sponsor or endorse, or are affiliated with or otherwise connected to, Capital Group Companies, Inc., or any of its products or services. All Index Data is provided for informational purposes only, on an “as available” basis, without any warranty of any kind, whether express or implied. Cliffwater and its affiliates do not accept any liability whatsoever for any errors or omissions in the Indexes or Index Data, or arising from any use of the Indexes or Index Data, and no third party may rely on any Indexes or Index Data referenced in this report. No further distribution of Index Data is permitted without the express written consent of Cliffwater. Any reference to or use of the Index or Index Data is subject to the further notices and disclaimers set forth from time to time on Cliffwater’s website at https://www.cliffwaterdirectlendingindex.com/disclosures.