President Trump’s tariffs have put market volatility back in the spotlight.

After tariffs on nearly all trading partners were announced on April 2, the S&P 500 Index briefly descended into bear market territory — a rare sign of extreme economic pessimism when stocks fall by 20% or more from their peak. A 90-day pause on reciprocal tariffs declared on April 9 caused the index to skyrocket 9.5%, only to fall 3.5% the following day.

The damage spilled over to the U.S. Treasury market, which may explain why Trump paused some tariffs. The yield on the 10-year Treasury, a cornerstone of the global financial system, widened to 4.34% from 4.01% a few days prior — an indication of market turbulence.

Given the uncertain environment, investors may have doubts about their investment approach. It’s natural to seek calmer shores when markets are choppy. But it’s equally important to step back, gain perspective and look toward the horizon.

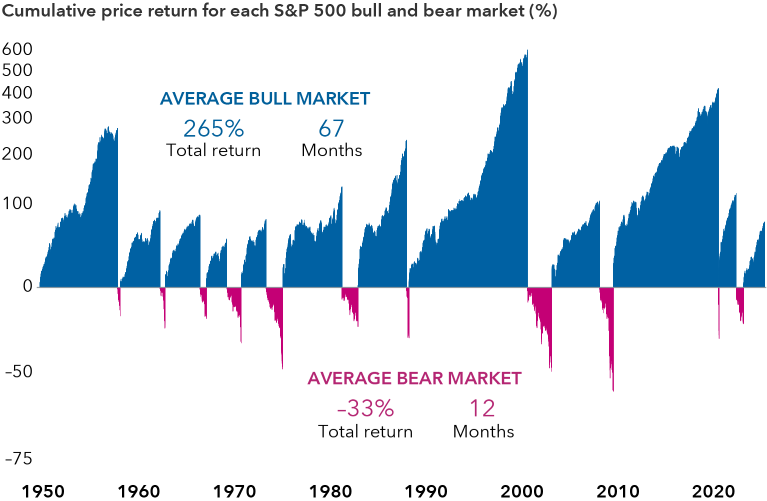

History shows the stock market has always recovered from previous declines, though there’s no guarantee downturns will lead to rebounds. Here are five insights that can help you regain confidence and stay invested for the long haul.