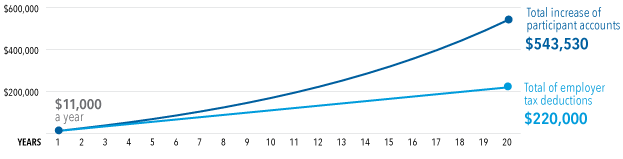

As annual 401(k) plan reviews approach, are you using all the tools in your toolbox to manage what could be challenging conversations? One idea you may not have considered is to demonstrate the potential tax advantages to employers that come from how plan expenses are paid.

Many 401(k)s are reflexively set up to pass on some plan costs to participants. And some plan sponsors may be unaware that other options exist. But paying some or all plan expenses out of company funds can have benefits for both employers and employees.